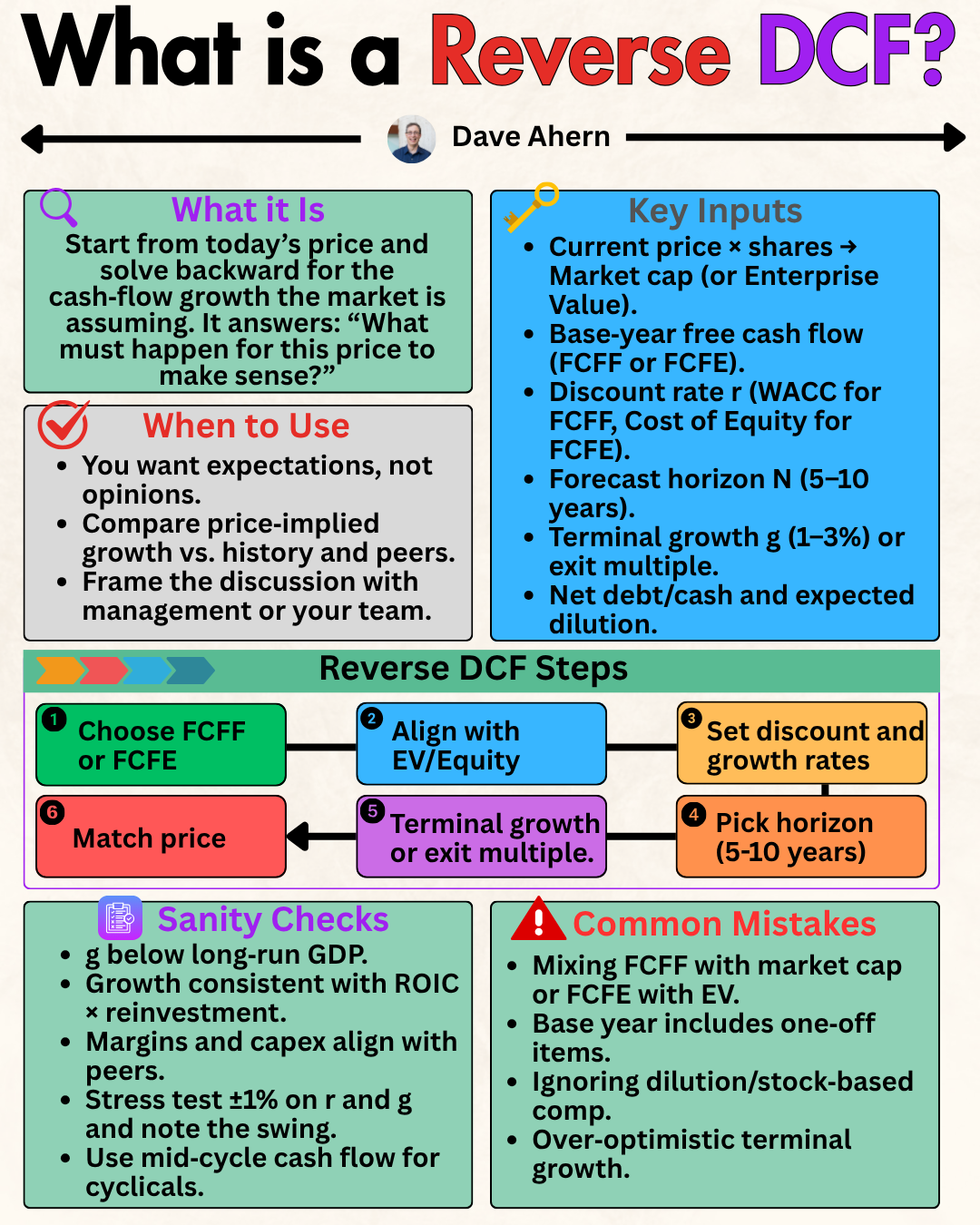

Reverse DCF, Demystified: A 5‑Step Visual Walkthrough Using Google (Alphabet)

Most DCFs start with your assumptions and end with a valuation.

Reverse DCFs flip it.

You start with the market price and work backward to the growth, margins, and reinvestment efficiency that the market is implying. In this guide, we’ll run a reverse DCF on Alphabet and demonstrate how to sanity-check the outputs through a quality-investing lens, including ROIC vs. WACC, reinvestment runway, FCF conversion, and moat evidence.

TL;DR

A reverse DCF converts today’s price into implied growth, margins, and capital intensity; it’s a bias‑reducing way to test plausibility.

Quality investors care about ROIC sustainably above WACC, ample reinvestment opportunities, and efficient FCF conversion.

Alphabet’s fundamentals provide multiple cross-checks: segment margins, TAC dynamics, capex intensity for AI/data centers, and per-share value creation through buybacks.

Decision rules: prefer ROIC – WACC > 5% sustained, stable FCF margins, and per‑share growth exceeding headline revenue growth.

Run three implied sets: “no‑heroics,” “base‑rate,” and “bull‑case runway,” then check against business reality (competition, regulation, AI infra needs).

Why it matters

Reverse DCFs answer the question: “What must be true for today’s price to be fair?” That’s powerful because:

It reduces “narrative bias.” You’re not anchoring on your favorite bull thesis; you’re testing the market’s embedded story.

It’s comparable across firms and cycles. Strip out multiple noise and go straight to cash economics.

It aligns with quality investing. You can immediately check if implied ROIC and reinvestment are realistic given the moat durability and capital intensity.

Where investors go wrong:

Using headline growth without linking to reinvestment needs. Growth consumes capital; reverse DCFs should tie growth ↔ margins ↔ asset turns.

Ignoring per‑share. Buybacks, SBC (stock-based compensation), and dilution alter per-share value creation.

Confusing the cost of capital. WACC is not a constant; it should be matched to business risk and leverage.

Core concepts

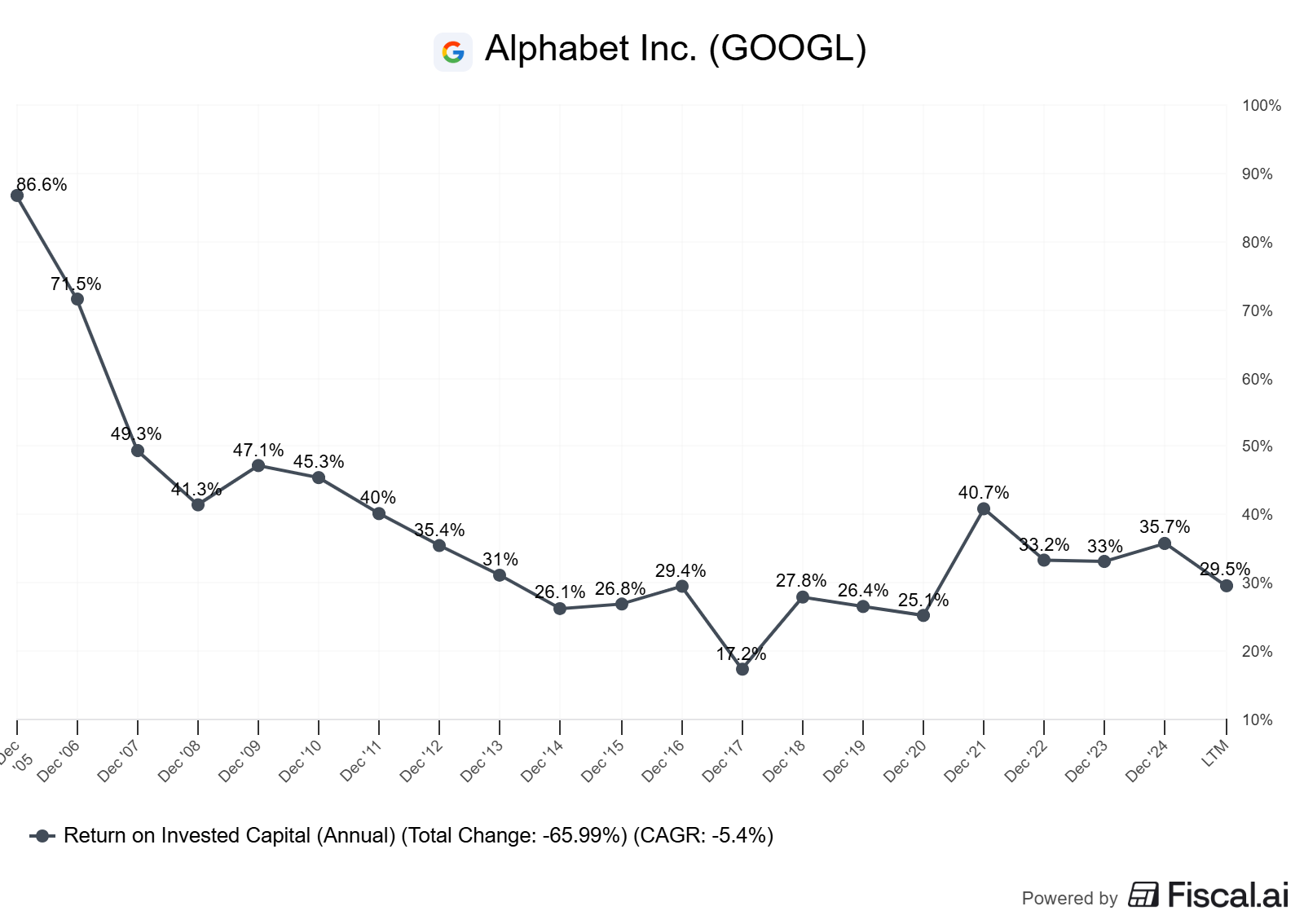

ROIC vs WACC and value creation

ROIC (return on invested capital) is the after‑tax operating return on the capital required to run the business. Value is created when ROIC > WACC (weighted average cost of capital).

Quality investors prefer a sustained spread, often looking for ROIC – WACC > 5% across cycles.

In reverse DCF, the key test is: are the implied margins/asset turns consistent with a ROIC that clears WACC, not just near‑term, but through the fade period?

Reinvestment runway and capital intensity

Growth requires incremental investment. For software/platforms, reinvestment is typically opex-heavy (people and R&D) and capex-light—except when infrastructure shifts (e.g., AI data centers) increase capex.

Tie implied growth to the reinvestment rate and incremental ROIC. If implied growth is high while capex and working capital needs are low, the DCF implicitly assumes unusually high incremental ROIC.

Unit economics and per‑share metrics

Unit economics (LTV/CAC, gross profit per incremental dollar, and TAC as a percentage of ads) reveal whether growth is profitable or subsidized.

Per‑share framing matters. Buybacks at or below intrinsic value accelerate per-share compounding; SBC can offset those gains.

Moat durability and evidence (not claims)

Look for evidence: stable or rising gross/operating margins, pricing power (ad auction dynamics), retention/switching costs (Search defaults, ecosystem gravity), and competitive outcomes (Cloud profitability turning positive).

Evidence beats claims; watch 5–10y trend bands.

Worked example: Alphabet

We’ll use Alphabet (Google) to demonstrate the technique and cross‑checks.

Key sources:

Alphabet FY2024 Form 10‑K for the year ended December 31, 2024, filed Feb 5, 2025. See the filing and share count disclosures Alphabet 2024 10‑K PDF and EDGAR HTML. Data “as of” 2024‑12‑31 unless noted.

Alphabet FY2024 Q4 earnings release for cash flows and repurchases context Alphabet FY2024 Earnings Release PDF. “As of” 2025‑02‑04.

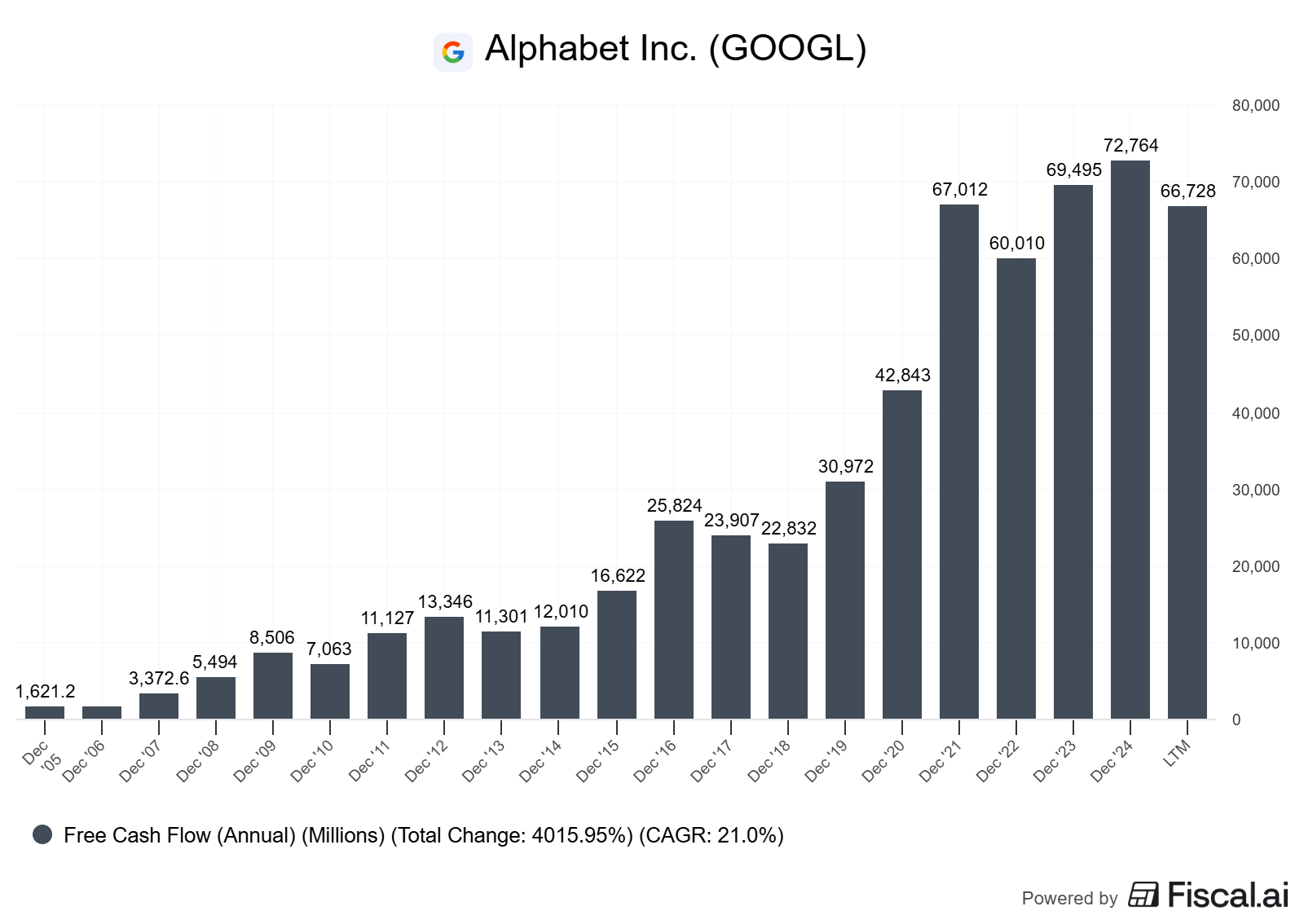

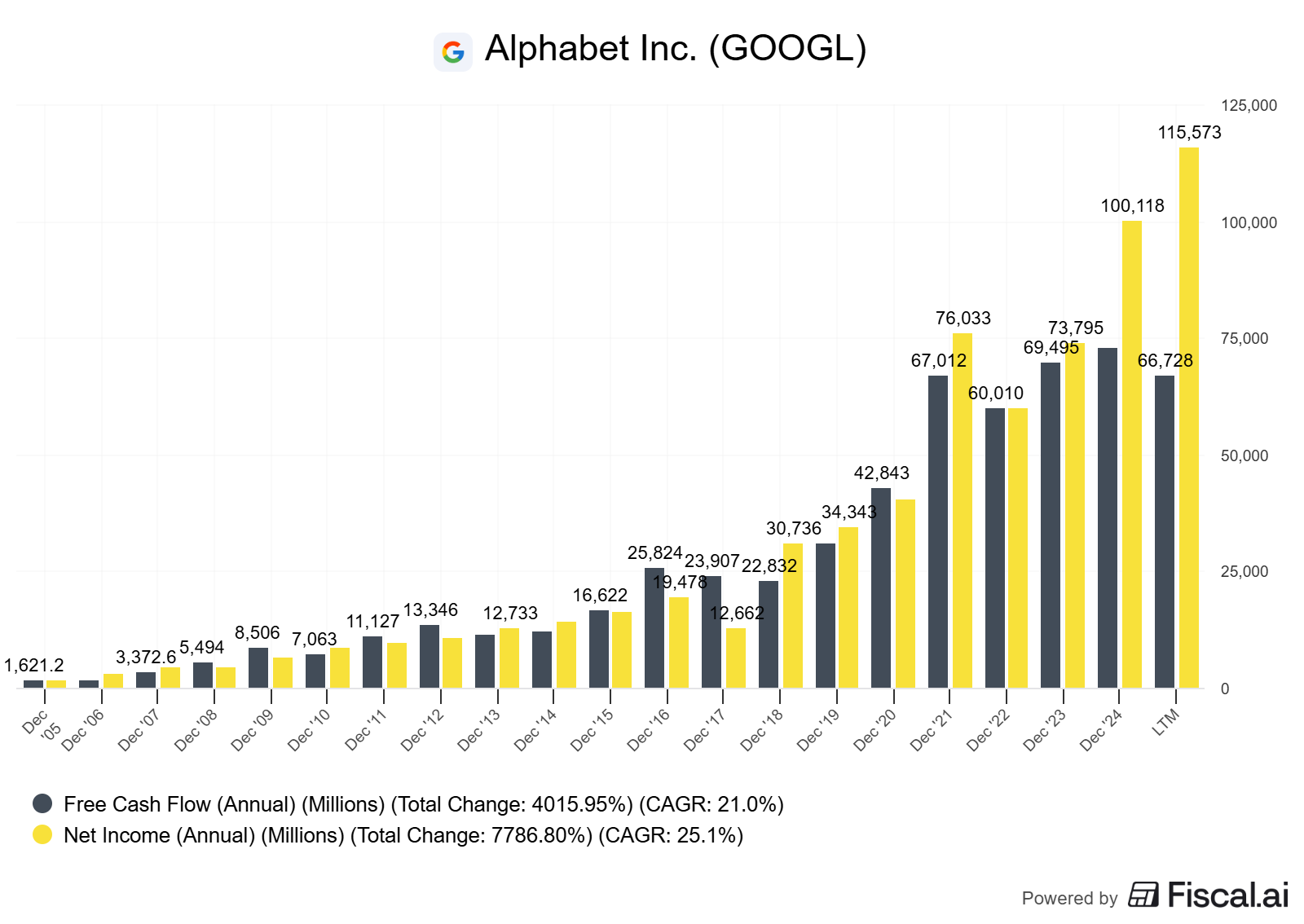

Step 1: Normalize base free cash flow (FCF)

FCF = Operating cash flow − Capital expenditures. Adjust for non‑recurring items; be explicit about SBC’s economic treatment (cash vs economic cost).

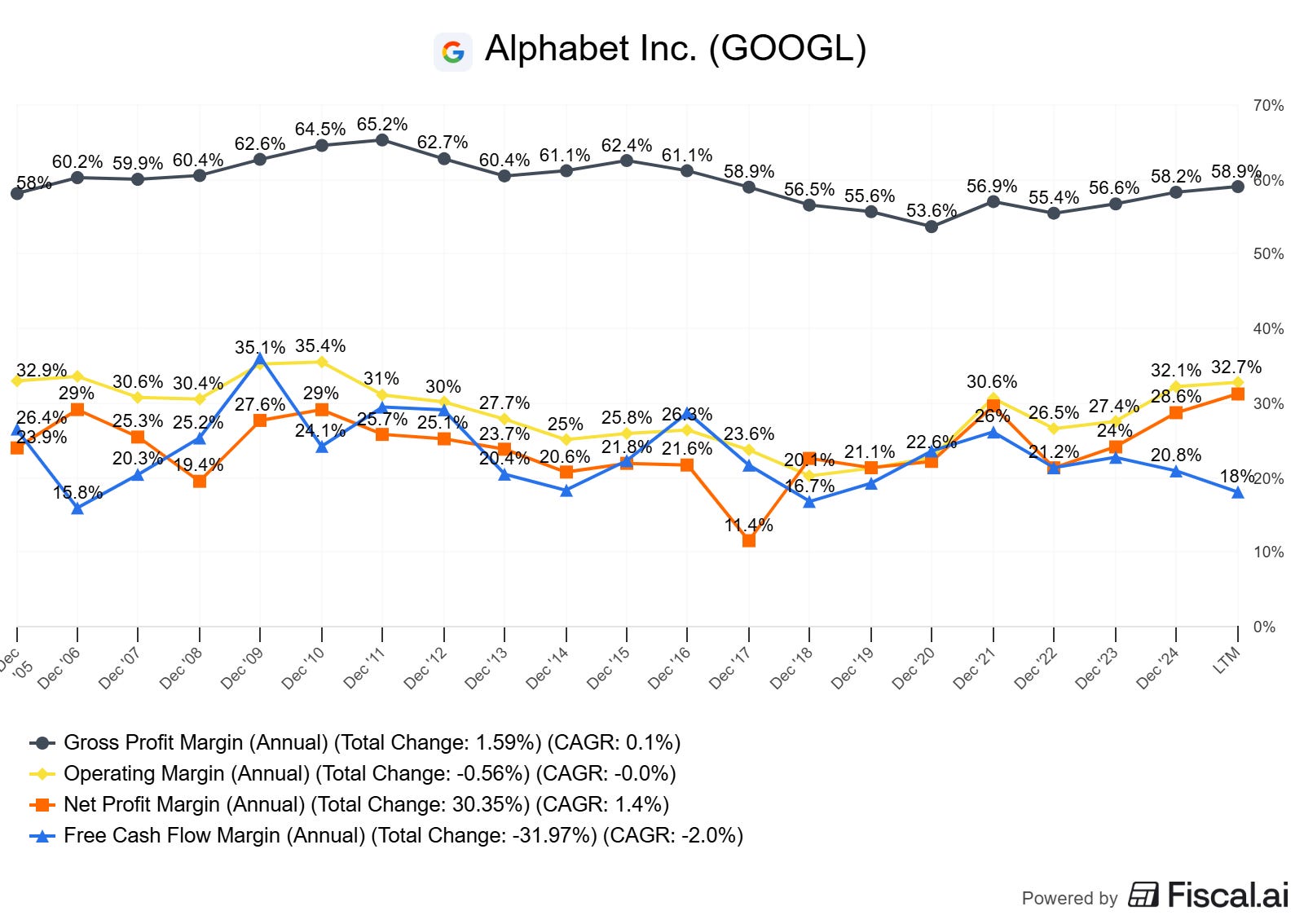

Cross-check Google Services vs Cloud dynamics: Cloud has recently become profitable, changing the consolidated FCF conversion. Use a 3–5 year average FCF margin to smooth AI-capex lumpiness.

Practical proxy: take FY2024 FCF and haircut/normalize for elevated capex cycle if you believe it’s above mid‑cycle needs. Document your choice.

Step 2: Choose an appropriate WACC

Use a range (e.g., 8–10%) to reflect interest rates, equity risk premium, and business risk. Alphabet’s net cash position and scale generally compress WACC vs smaller peers. Justify your range with market inputs, not precision theater.

Step 3: Set horizon and terminal/fade

Use 10 years with a fade from near‑term growth to a steady terminal growth (g) consistent with long‑run nominal GDP (e.g., 2–3% in USD).

Make the fade explicit: growth and excess ROIC decline gradually (“fade”) toward maturity.

Step 4: Back into implied assumptions from price

Mechanically, solve for the FCF growth path (and/or margin expansion and reinvestment rates) that discount to today’s enterprise value (EV). Then translate that growth path into operational assumptions: revenue growth, operating margin, capex/working capital intensity.

Show three implied sets that all reconcile to price: “no‑heroics,” “base‑rate,” and “bull runway.”

Step 5: Sanity‑check with quality metrics

ROIC vs WACC: Are the implied margins and asset turns compatible with ROIC sustainably clearing WACC?

Reinvestment runway: Do segment opportunities (Search, YouTube, Cloud, Other) justify implied growth without heroic TAM leaps?

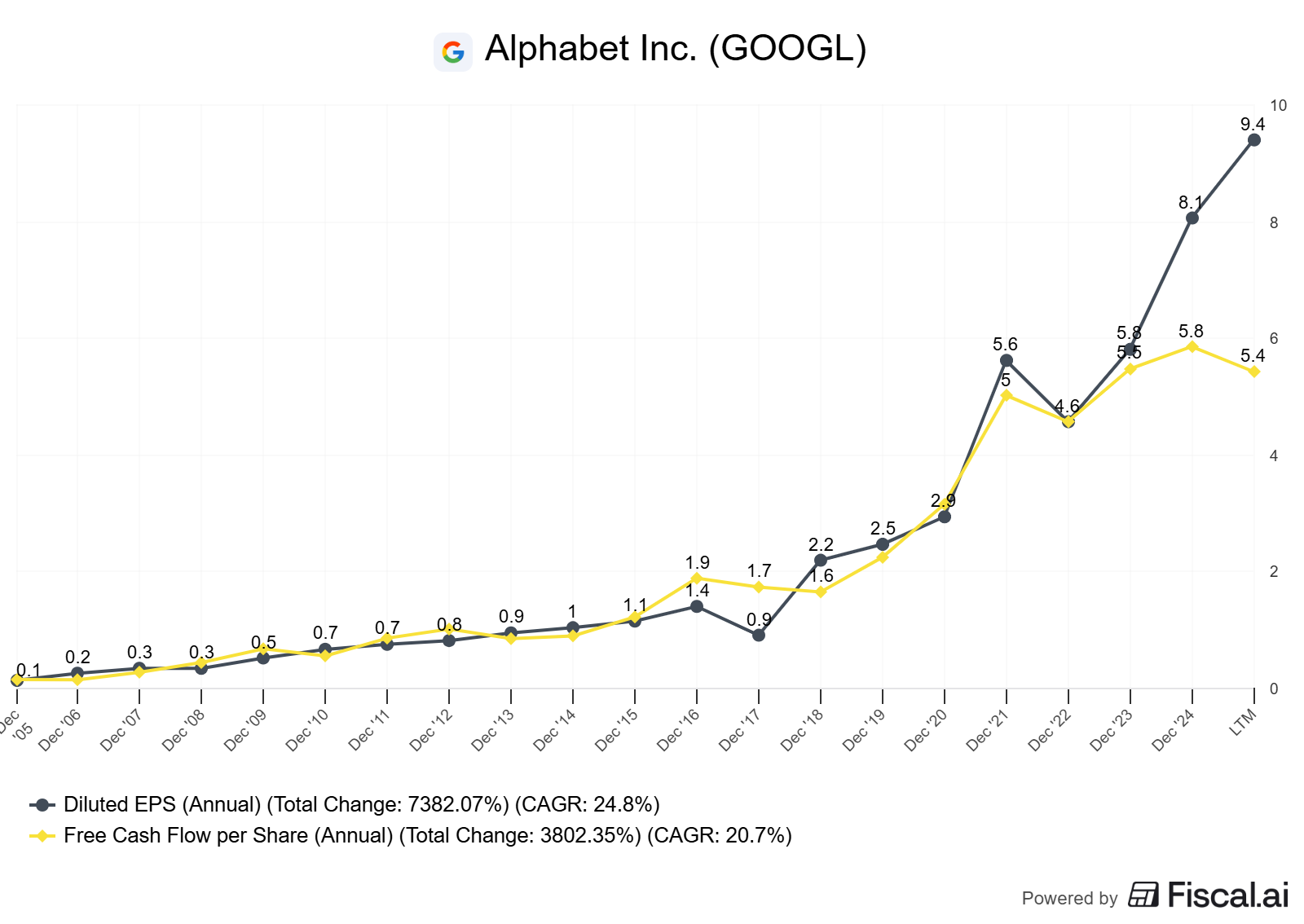

Per‑share: Do buybacks offset SBC and shrink the denominator? Are repurchases done at prices below or near intrinsic value?

Moat durability: Do 5–10y trend bands show margin resilience despite competition/regulatory friction?

What Alphabet’s filings help you verify

Revenue mix and growth (Search/YouTube vs Cloud) [10‑K, Business/Segments; “as of” 2024‑12‑31].

Cash flow, capex trajectory, and stock repurchases (with cash paid for repurchases cited in quarterly/fiscal releases) [FY2024 Earnings Release; “as of” 2025‑02‑04].

Share counts (Class A/B/C; diluted weighted average in FS) [10‑K; “as of” 2024‑12‑31].

Caveats and alternative interpretations

AI infrastructure capex is a moving target; “normalized” capex may stay elevated longer than expected as models and workloads grow.

Cloud mix shift: as Cloud scale increases, consolidated margins and FCF margins can step‑change; timing matters.

Regulation and default search economics can alter TAC and monetization, affecting margin stability.

Here are some hypothetical scenarios to illustrate this in action.

Assume EV today is $2.1T, a normalized starting free cash flow (FCF0) of $95B, WACC of 9%, a 10-year horizon with a fade to maturity, a terminal growth rate of 2.5% (except where noted), net share count shrinking roughly 1% per year due to buybacks exceeding SBC dilution, and SBC treated economically in per-share framing. These are illustrative only, not forecasts.

No heroics: In this conservative setup, the price can be reconciled if FCF grows at about 6% annually for the first five years, then declines to roughly 3.5% by year 10, with a terminal growth rate of 2.5%. FCF margins remain essentially flat at around 24–25% as AI/data center capex absorbs much of the operating leverage.

This implies a reinvestment rate of around 25–30% at an incremental ROIC of roughly 18–20%, so most of the growth is reinvestment-led early on and gradually slows as opportunities mature. With margins stable, revenue growth is broadly similar to FCF growth in the mid-single digits during the first half of the horizon. Buybacks shrink the share count about 1% per year, lifting per‑share FCF growth to roughly 7% in the early years.

Quality-wise, the ROIC–WACC spread sits near 9–11%, which is healthy but not heroic, and the story assumes steady FCF conversion with realistic capital intensity in an ongoing AI investment cycle rather than outsized operating leverage.

Base-rate: A more typical large-cap compounding path reconciles the same price if FCF compounds at roughly 9% per year in years 1–5 and then declines to about 5% by years 6–10, with a 2.5% terminal growth rate. Here, FCF margin expands from about 25% to 27–28% by the back half of the decade as Cloud scales and YouTube/subscriptions mix in, allowing FCF growth to outpace revenue.

The implied reinvestment rate is closer to 35% at around 20% incremental ROIC, which yields approximately 7% reinvestment-driven growth early on, with the remaining lift coming from modest operating leverage. That margin expansion means revenue CAGR might land in the 6.5–7.5% range while FCF grows around 9%. With a roughly 1% annual share shrink, early per-share FCF growth approaches 10%.

The quality check still clears comfortably: a ~11% ROIC–WACC spread supports mid/high single-digit organic growth, and the scenario assumes Cloud profitability improves with scale while TAC and regulatory friction are absorbed without blowing out the margin bands.

Bull runway: A higher-quality runway with deeper operating leverage can also be reconciled to the same price if FCF grows roughly 12% per year for the first five years, then fades to about 7% in years 6–10, and has a slightly higher terminal growth rate of 3.0%. This path envisions FCF margins rising from around 25% to 30–31% by year 10, reflecting sustained efficiency gains and a more diversified mix of cloud and AI services. It implies a reinvestment rate of about 40% at roughly 25% incremental ROIC, meaning around 10% organic growth early from reinvestment alone, with another ~2% from operating leverage.

Under those assumptions, revenue might grow in the 9–10% range, while FCF does ~12%, and with buybacks shrinking the share count by ~2% annually, per-share FCF growth could approach 14% in the early years. The quality bar is high: it requires a robust, durable moat with strong ad pricing/engagement, a sustained cloud win rate translating into scale economics, and AI capex converting efficiently into high-return workloads to hold a ~16% ROIC–WACC spread through the fade.

A quick sensitivity note: if the WACC rises to 10% from 9%, each scenario typically requires roughly one to two percentage points more early FCF growth (or approximately 100–150 bps more terminal margin) to reconcile. If WACC falls to 8%, you can trim one to two points of early FCF growth or assume ~100 bps less margin expansion. Similarly, raising terminal growth from 2.5% to 3.0% relaxes the required early FCF growth by about half to one point, while cutting terminal growth to 2.0% tightens it by a similar amount.

Finally, if your “normalized” FCF0 was actually closer to $85B than $95B, you’d generally need an extra ~1.5–2 points of early FCF growth (or faster margin gains) to hit the same enterprise value under each story.

How to do this yourself

Step‑by‑step

Gather data

Income statement, cash flow, segment info, share counts: company 10‑K/10‑Q and earnings releases. Alphabet: Investor Relations and FY2024 10‑K PDF. “As of” 2024‑12‑31.

Market cap, net cash/debt: latest quarter and price from your data provider; compute EV = Market Cap + Net Debt − Non‑operating assets.

Capex and working capital trends to estimate reinvestment needs.

Normalize FCF

Compute FCF = CFO − Capex. Build a 3–5y average FCF margin to smooth cycle noise.

Decide SBC treatment. Economic purists subtract an SBC “cash‑equivalent” charge (or model dilution explicitly via per‑share).

Set capital costs and horizon

Pick WACC range (e.g., 8–10% for large‑cap, net‑cash, global platforms).

Horizon: 10 years with a fade into terminal growth (g = 2–3%). Document your base CPI/GDP assumptions.

Solve for implied operations

Use today’s EV and discount schedule to back into the FCF path that reconciles to price.

Translate that FCF path into operating assumptions: revenue growth, operating margin trajectory, reinvestment rate (Reinvestment = Growth / ROIC), and capital intensity.

Cross‑check with quality metrics

Decision rules and thresholds:

Prefer ROIC – WACC > 5% sustained (mid‑cycle).

Avoid cases where implied growth requires implausibly low reinvestment relative to historical capex/working capital.

Per‑share: Favor shrinking diluted share counts (>1%/yr) with SBC under control and buybacks at reasonable prices.

FCF conversion: Prefer FCF margin stability or improvement, not perpetual compression.

Build three “implied” scenarios

No‑heroics: Modest growth, stable margins, terminal g at 2%. Does price already assume this?

Base‑rate: Industry/peer‑informed growth with gradual margin expansion and Cloud mix uplift.

Bull runway: Higher reinvestment, Cloud profitability scale, durable ad monetization; terminal ROIC still > WACC.

What to calculate

ROIC: NOPAT / Invested Capital. Define NOPAT as operating income × (1 − tax rate); Invested Capital as operating assets − operating liabilities (or equity + net debt − non‑operating assets).

Incremental ROIC: ΔNOPAT / ΔInvested Capital (more indicative of runway quality).

Growth implied: g ≈ Reinvestment Rate × ROIC (sanity check your reverse DCF growth path).

Pitfalls and false positives

Treating SBC as “free.” SBC dilutes per‑share value even if cashless. Either reduce FCF by a SBC “replacement” charge or model dilution explicitly.

Ignoring capital intensity shifts. AI‑era infra raises capex; assuming pre‑AI capex permanently can overstate steady‑state FCF.

Over‑optimistic terminal assumptions. Terminal g above nominal GDP or permanent supra‑normal ROIC invites errors unless justified by exceptional moat durability.

Not reconciling to segments. Cloud profitability inflection and YouTube/Subscriptions mix can change consolidated margins.

Using EV multiples as destiny. Multiples are a symptom; reverse DCF forces the operating cause.

Checklist / one‑pager

Price to EV computed with latest net cash/debt.

Base FCF normalized (3–5y), SBC treatment explicit.

WACC range established (e.g., 8–10%).

10y horizon with fade; terminal g in 2–3%.

Three implied paths reconciled to EV with clear growth, margin, reinvestment, and terminal assumptions.

ROIC – WACC spread > 5% sustained preferred.

FCF conversion trend acceptable; capex path realistic for AI infra.

Per‑share metrics: FCF/share, EPS, share count, SBC/dilution vs buybacks.

Moat evidence: margin band stability, pricing power, retention/switching costs, competitive outcomes (e.g., Cloud operating income inflection).

Red flags documented (regulatory, TAC shifts, competition).

Glossary

Reverse DCF: Valuation by inferring growth/margins from current price.

ROIC: NOPAT divided by invested capital, measuring operating return on capital.

WACC: Weighted cost of equity and after‑tax debt, reflecting overall capital cost.

FCF: Free cash flow, operating cash flow minus capex (after adjustments).

TAC: Traffic acquisition costs; payments to partners to source traffic.

Terminal growth (g): Perpetual growth rate applied after the explicit forecast period.

Incremental ROIC: Return on newly invested capital; a better proxy for runway quality.

SBC: Stock‑based compensation; non‑cash expense with dilution economics.

Further reading

Alphabet Inc. FY2024 Form 10‑K and investor materials (as of 2024‑12‑31; filed 2025‑02‑05): 10‑K PDF, EDGAR HTML, Investor page.

Alphabet FY2024 Q4 earnings release (as of 2025‑02‑04): PDF.

On ROIC and value creation: McKinsey, “Valuation: Measuring and Managing the Value of Companies.”

Aswath Damodaran, papers on DCF, growth, and cost of capital (NYU).

References

Alphabet Inc. Form 10‑K for fiscal year ended 2024‑12‑31, filed 2025‑02‑05. Includes business overview, segment disclosure, share counts, and risk factors. Alphabet 2024 10‑K PDF (as of 2024‑12‑31).

Alphabet Inc. FY2024 Q4 Earnings Release, Workiva PDF (includes cash paid for stock repurchases, revenue commentary). Alphabet FY2024 Earnings Release (as of 2025‑02‑04).

EDGAR HTML version of Alphabet FY2024 10‑K. SEC EDGAR (as of 2024‑12‑31).

Alphabet Investor Relations hub (earnings, filings, slides). IR site (as of 2025‑09‑05).