Reading Between the Lines: What Dividend Increases (and Cuts) Tell You About a Business

“The best thing a company can do with its money is reinvest it at high rates of return. The second best thing is to return it to shareholders.”

— Warren Buffett

Most investors view a dividend as income. A quarterly check. A yield percentage on a screener. But a dividend decision is actually one of the loudest signals management sends about what’s happening inside the business.

When a company raises its dividend, management is telling you something. When a company cuts its dividend, management is screaming something. And when a company pays a suspiciously high yield while the business deteriorates underneath it, the market is waving a red flag that too many investors mistake for a green one.

In today’s post, we will learn:

Why Dividend Decisions Are a Signal, Not Just Income

What a Dividend Increase Really Tells You

The Anatomy of a Dividend Cut (and What It Reveals)

The High-Yield Trap: When a Big Dividend Is a Warning

How to Use Dividend Signals in Your Investing Process

Let’s dive in and learn how to read between the lines of a company’s dividend policy.

Why Dividend Decisions Are a Signal, Not Just Income

Before we get into the specifics, let’s establish why dividend decisions matter beyond the income they provide.

A dividend is a capital allocation decision. Every dollar a company pays as a dividend is a dollar it chose not to reinvest in the business, use for acquisitions, pay down debt, or buy back shares. That choice tells you how management views its own opportunities.

Think of it this way. If the CEO of a company could reinvest every dollar at 25% returns, why would they send that dollar to you? They wouldn’t. They’d reinvest it and compound your wealth faster than any dividend could.

But if the CEO sees diminishing reinvestment opportunities, returning cash to shareholders becomes the responsible move. Buffett himself resisted paying a dividend at Berkshire Hathaway for decades because he believed he could allocate capital more effectively than shareholders could on their own. That’s a signal of confidence in reinvestment opportunities.

The key insight is this: dividends aren’t inherently good or bad. What matters is the context. A dividend increase from a company generating growing free cash flow with a low payout ratio signals strength. Maintaining a dividend at all costs while debt rises and cash flow declines signals trouble.

Let’s break down each scenario.

What a Dividend Increase Really Tells You

A dividend increase, especially a consistent pattern of increases over many years, tells you three things about a business.

First, management has confidence in future cash flows. A board of directors doesn’t raise the dividend unless it believes the business can sustain and grow those payments. Unlike a one-time buyback, a dividend increase creates an ongoing obligation. Cutting it later carries severe consequences (more on that shortly). So raising it is a statement: we expect the cash to keep flowing.

Second, the business is generating more cash than it needs to operate and grow. This is the crucial part. A company that raises its dividend while also reinvesting in the business at attractive rates of return is showing you a high-quality capital allocation engine at work. It’s not choosing between growth and dividends. It’s doing both.

Third, the company likely has pricing power and competitive advantages. Sustained dividend growth over decades requires sustained earnings growth. And sustained earnings growth requires a moat. Companies without pricing power or competitive advantages cannot grow earnings consistently enough to raise dividends for 10, 20, or 50 consecutive years.

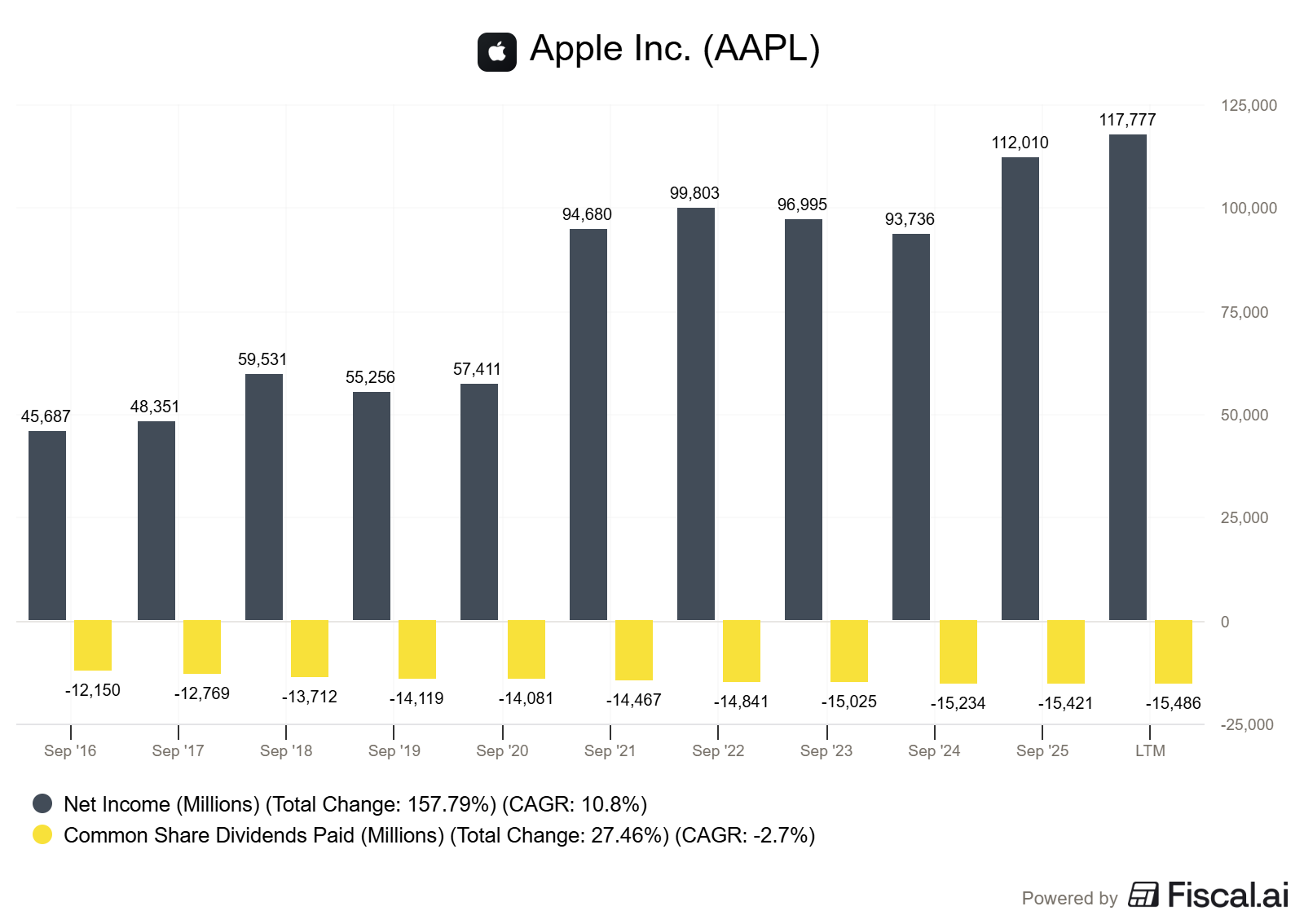

Apple: A Case Study in Dividend Growth as a Strength Signal

Apple (AAPL) reinstated its dividend in 2012 after a 17-year hiatus. At the time, the company was sitting on an enormous and growing cash pile. The reinstatement and subsequent annual increases weren’t a sign that Apple had run out of ideas. They signaled that the business was generating so much free cash flow that it could fund massive R&D, repurchase billions in stock, and still raise the dividend every year.

According to Apple’s fiscal year 2024 10-K (filed with the SEC), Apple generated approximately $108.3 billion in cash from operations on $391 billion in net sales. The company paid approximately $15.2 billion in dividends that year. That’s a payout ratio against operating cash flow of roughly 14%.

That low payout ratio combined with consistent increases tells you something powerful: Apple’s dividend is well-covered, growing, and represents a small fraction of the cash the business produces. The dividend increase isn’t straining the business. It’s a byproduct of a machine that generates far more cash than it needs.

What to Look For in a Healthy Dividend Increase

When evaluating whether a dividend increase is a genuine sign of strength, check these metrics:

Free cash flow payout ratio below 60%. This means the company is paying out less than 60% of its free cash flow as dividends, leaving room for reinvestment, debt reduction, and buybacks. Calculate this by dividing total dividends paid (from the cash flow statement) by free cash flow (operating cash flow minus capital expenditures).

Revenue and earnings growth alongside dividend growth. If dividends are growing faster than the underlying business, that’s a yellow flag. The payout ratio will eventually catch up.

Stable or declining debt levels. A company funding dividend increases by taking on more debt is borrowing from the future to pay you today. That’s not sustainable.

Consistent ROIC above the cost of capital. As we’ve discussed in previous articles, this tells you the business is creating value, not just moving money around.

The Anatomy of a Dividend Cut (and What It Reveals)

If a dividend increase is a confident whisper, a dividend cut is an alarm bell.

Companies avoid cutting dividends at almost any cost. Management teams know that a cut signals distress, triggers selling from income-focused funds, and damages their credibility with shareholders. So when they do cut, it usually means things have gotten bad enough that they have no choice.

A dividend cut tells you:

Cash flow has deteriorated significantly. The business is no longer generating enough cash to sustain the payout. This could be cyclical (a temporary downturn) or structural (the business model is under pressure). The distinction matters enormously.

Management’s prior confidence was misplaced. Remember, every dividend increase is an implicit promise that cash flows will support the higher payment. A cut is an admission that the promise was broken.

The balance sheet may be under stress. Companies often cut dividends to preserve cash when debt becomes unmanageable. If you see a dividend cut alongside rising debt and declining cash flow, that’s a business in serious trouble.

AT&T: When a High-Yield Masked Declining Fundamentals

AT&T (T) provides one of the most instructive examples of a dividend cut in recent memory. For years, AT&T was considered a blue-chip income stock. The company had raised or maintained its dividend for over 30 consecutive years. Income investors loved the yield, which hovered around 7% to 8% in the years before the cut.

But the fundamentals told a different story.

According to AT&T’s fiscal year 2021 10-K (filed with the SEC), the company carried approximately $178.6 billion in total debt (including long-term debt, short-term debt, and finance lease obligations). The company’s free cash flow had been under pressure for years as it tried to integrate its massive acquisitions (DirecTV, Time Warner) while also investing heavily in 5G infrastructure and fiber buildout.

In early 2022, AT&T cut its dividend by approximately 47% in connection with the spin-off of its WarnerMedia business. The cut was framed as a strategic reset, but the underlying message was clear: the company had been paying out more than it could sustainably afford while carrying an enormous debt load.

The warning signs were visible years before the cut:

Debt levels were staggering. As we detailed in our article on the market value of debt, AT&T’s total debt in fiscal 2022 was approximately $154.7 billion. The weighted average maturity of that debt was over 37 years, locking the company into interest payments for decades.

Dividend obligations were consuming free cash flow. The payout ratio against free cash flow had been climbing, leaving less room for debt reduction or reinvestment.

ROIC was mediocre relative to the capital deployed. When a company deploys that much capital through acquisitions and infrastructure and generates modest returns, the math eventually catches up.

The lesson here isn’t that AT&T is a bad company. It’s that the dividend yield was masking fundamental business challenges. Investors who focused only on the yield missed what the balance sheet and cash flow statement were telling them.

The High-Yield Trap: When a Big Dividend Is a Warning

This brings us to one of the most dangerous traps in dividend investing: the high-yield trap.

Here’s how it works. A company’s stock price declines because the market perceives deteriorating fundamentals. As the stock price falls, the dividend yield rises (because yield equals annual dividend divided by stock price). Income-seeking investors see the high yield and buy, thinking they’re getting a bargain. Then the dividend is cut, the stock drops further, and those investors suffer both income and capital losses.

The yield is high because the market is pricing in a cut. The market isn’t always right, but when you see a yield significantly above the sector average, your first instinct should be skepticism, not excitement.

A useful rule of thumb: if a company’s yield is more than double the sector average, investigate why before assuming it’s an opportunity.

How to Spot the High-Yield Trap

Look for these warning signs:

Free cash flow payout ratio above 80%. At this level, there’s almost no margin for error. Any decline in cash flow threatens the dividend.

Declining revenues over multiple years. A shrinking top line makes it progressively harder to support fixed dividend obligations.

Rising debt to fund operations (not growth). If the company is borrowing to maintain the business rather than expand it, the dividend is living on borrowed time. Literally.

Management repeatedly emphasizes its “commitment” to the dividend. Ironically, when management starts aggressively defending the dividend on earnings calls, it’s often because analysts are questioning its sustainability. Healthy dividends don’t need defending.

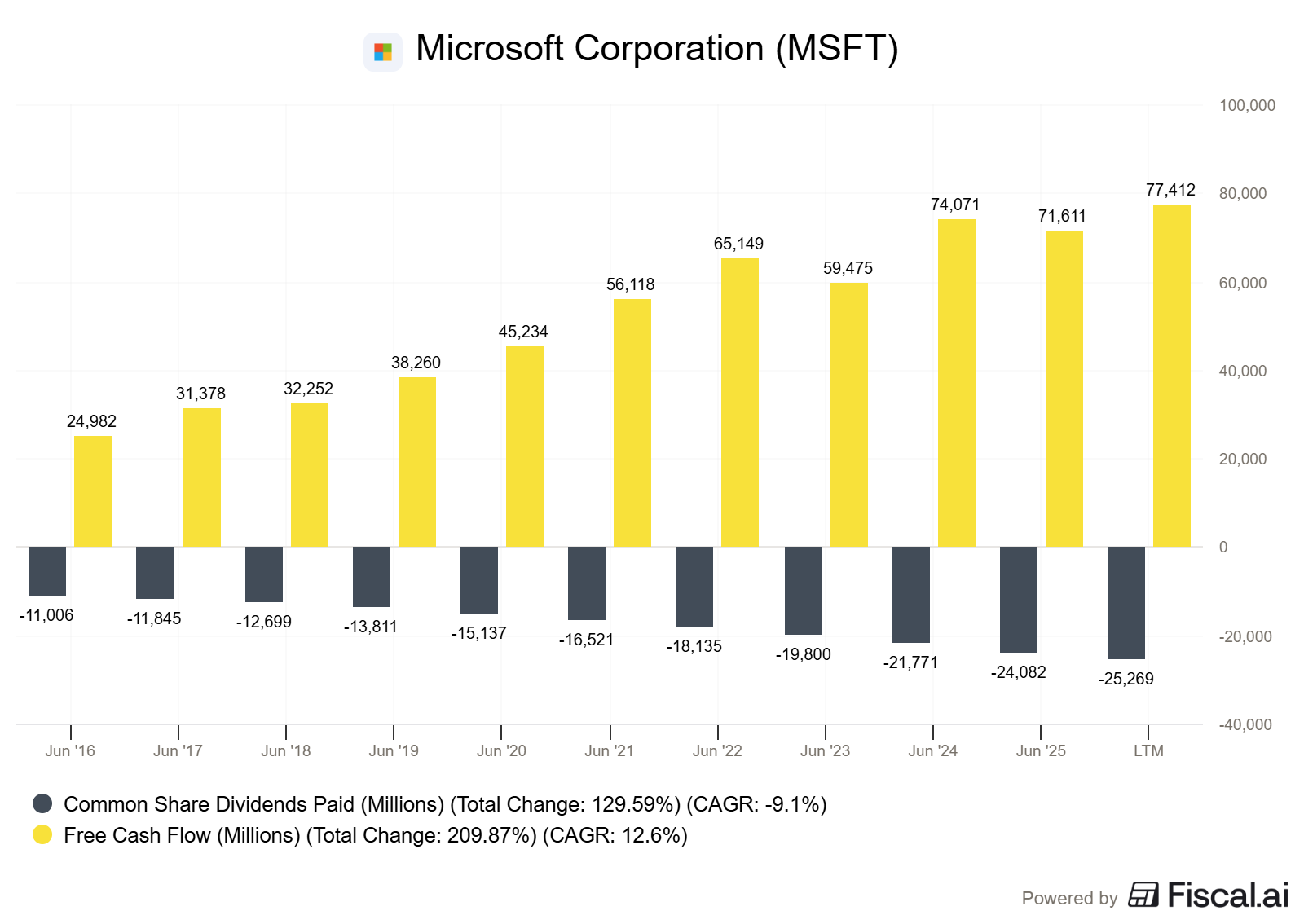

Contrast: Microsoft’s Dividend as a Strength Signal

Compare the AT&T scenario with Microsoft (MSFT). Microsoft has raised its dividend consistently since initiating it in 2003. According to Microsoft’s fiscal year 2024 10-K (filed with the SEC for the fiscal year ending June 30, 2024), the company generated approximately $118.5 billion in cash from operations. Total dividends paid were approximately $21.8 billion.

Microsoft’s yield has typically been modest (usually between 0.7% and 1.2% in recent years) because the stock price keeps rising alongside earnings growth. The low yield isn’t a weakness. It’s a reflection of a business compounding so effectively that the stock price growth outpaces the dividend growth.

This is the kind of dividend you want: one that grows every year, is comfortably covered by cash flow, and represents a small fraction of the value the business creates.

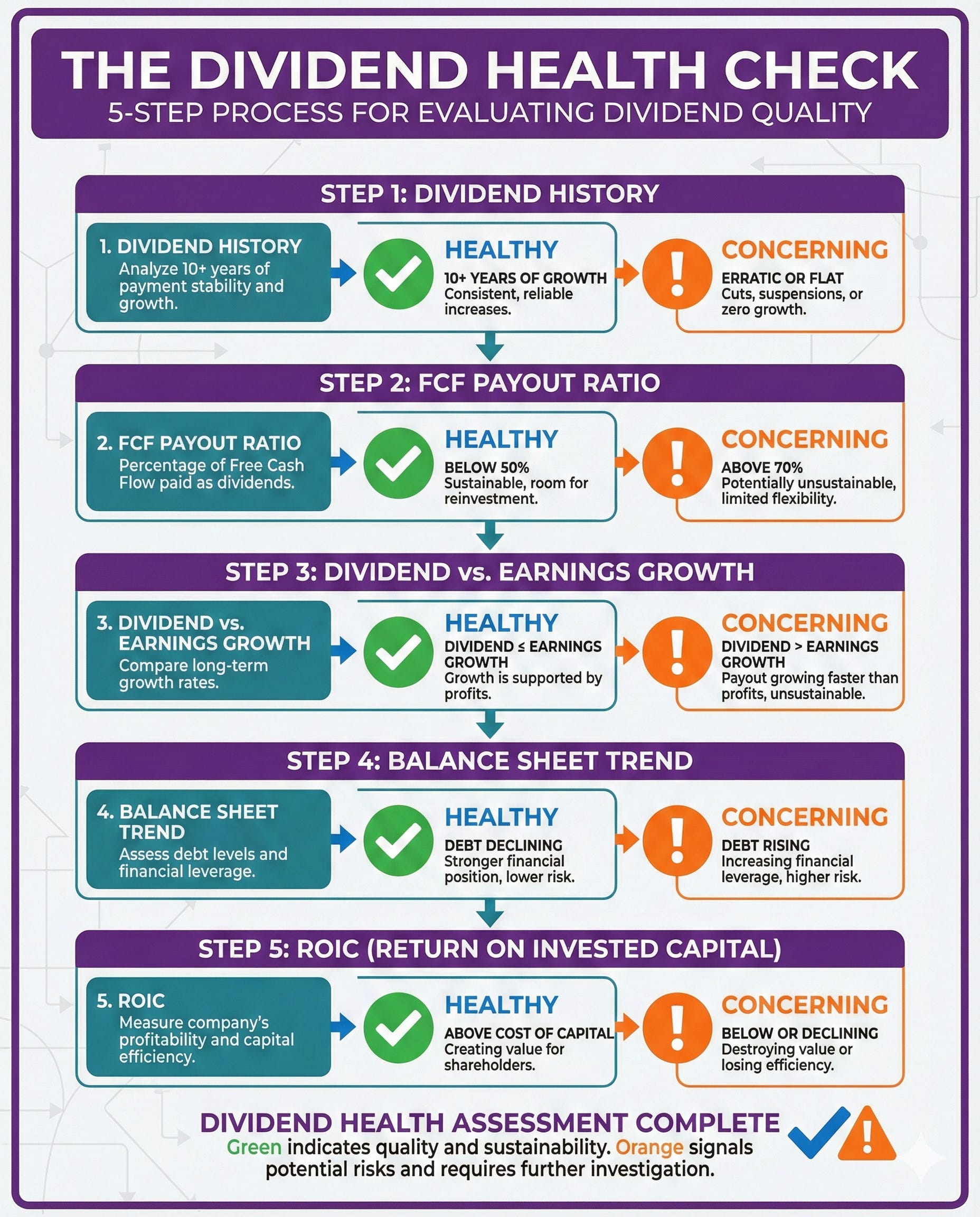

How to Use Dividend Signals in Your Investing Process

Here’s how to put all of this into practice when you’re evaluating a company.

Step 1: Look at the dividend history. Go to the company’s investor relations page or SEC filings and look at at least 10 years of dividend payments. Is the dividend growing? Flat? Erratic? The pattern itself is a signal. Companies with 10+ consecutive years of dividend growth have demonstrated sustained earnings power.

Step 2: Calculate the free cash flow payout ratio. Pull total dividends paid from the cash flow statement. Calculate free cash flow (operating cash flow minus capital expenditures). Divide dividends by free cash flow. If the ratio is below 50%, the dividend is well-covered. Between 50% and 70%, it’s adequate, but watch the trend. Above 70%, dig deeper into whether cash flows are stable enough to sustain it.

Step 3: Compare dividend growth to earnings and revenue growth. If dividends are growing at 8% annually but earnings are growing at 3%, the payout ratio is expanding. That’s unsustainable over time. The best-case scenario is dividend growth at or below earnings growth, indicating a stable or improving payout ratio.

Step 4: Check the balance sheet. Look at total debt, net debt (total debt minus cash), and how debt levels have trended over the period of dividend growth. A company that’s growing its dividend while reducing debt demonstrates exceptional financial discipline. A company growing its dividend while adding debt deserves more scrutiny.

Step 5: Evaluate ROIC alongside the dividend. As we’ve covered extensively, ROIC tells you whether the company is creating value with the capital it retains. A company with high ROIC and a growing dividend is the best of both worlds: it’s reinvesting at attractive rates and still returning cash to shareholders. A company with declining ROIC and a growing dividend may be returning cash because it has no better use for it, which is a weaker (though not necessarily bad) signal.

Common Mistakes Investors Make with Dividends

Chasing yield over quality. A 7% yield from a struggling business is not better than a 1.5% yield from a compounder. The compounder will likely deliver better total returns (capital appreciation plus growing dividends) over any meaningful time period.

Ignoring the payout ratio. A dividend that consumes 90% of free cash flow might look great today, but it leaves the company no room to invest in growth, pay down debt, or weather a downturn.

Treating the dividend as guaranteed. There is no such thing as a guaranteed dividend. Even companies with 25+ year streaks of increases (the so-called Dividend Aristocrats) can and do cut when circumstances demand it.

Overlooking what’s not being paid. Sometimes the absence of a dividend is the most bullish signal of all. When Berkshire Hathaway retains all its earnings, it’s because Buffett believes he can compound that capital at higher rates than shareholders could earn elsewhere. If ROIC supports that view, the lack of a dividend is a feature, not a bug.

Investor Takeaway

Dividends are more than income. They’re a window into how management views the business's health and future.

A growing dividend backed by growing free cash flow, a low payout ratio, and strong ROIC tells you the business is healthy, and management is confident. A high yield with a deteriorating balance sheet and declining cash flow tells you the market sees trouble ahead, even if the checks are still arriving.

The single best habit you can develop is to look past the yield and ask: can this company afford to pay this dividend, grow it, and still invest in the business? If the answer is yes, you’ve likely found a quality company. If the answer requires assumptions, rationalizations, or hope, keep looking.

As always, thank you for taking the time to read this post, and I hope you find something of value on your investing journey.

If I can further assist, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave