Position Sizing Made Simple: How Much to Invest in Each Stock

You’ve done the hard work.

You’ve analyzed the business model, studied the financials, assessed the competitive moat, run your DCF model, and determined the stock is undervalued. You’re convinced this is a quality company trading at an attractive price.

Now comes the question that stumps even experienced investors:

How much should I actually invest in this stock?

This is where theory meets reality, where the rubber meets the road. And where many investors, who’ve mastered financial analysis, struggle.

I see it constantly. Investors who can eloquently explain why a company has pricing power, but put 2% in their highest-conviction idea and 8% in something they’re lukewarm about. Or worse, they size every position equally at 5% because “that seems diversified.”

Here’s the truth: Position sizing is where analysis becomes returns.

You can be right about a stock, but if you sized it at 1%, being right doesn’t matter. Conversely, you can have a mediocre pick sized at 15%, and being slightly wrong becomes painful.

Today, I’m walking you through a practical framework for position sizing that synthesizes two powerful approaches: conviction weighting and risk-based sizing. No complicated math. No academic theories you’ll never use. Just actionable methods you can implement in your portfolio this weekend.

Let’s dive in.

The Position Sizing Problem Nobody Talks About

Most investing education focuses on what to buy. Entire books dissect how to analyze balance sheets, competitive advantages, and management quality. But position sizing? It gets a paragraph. Maybe a chapter if you’re lucky.

This is backwards.

Position sizing is the multiplier on all your analytical work. It determines whether your great stock pick moves the needle or gets lost in the noise of your portfolio.

Consider two investors who both identify Applied Materials as undervalued in early 2023:

Investor A puts 3% of their portfolio in AMAT

Investor B puts 10% of their portfolio in AMAT

Fast forward 18 months. AMAT is up 60%.

Investor A’s portfolio is up 1.8% from this position

Investor B’s portfolio is up 6% from this position

Same stock. Same analysis. Different outcomes entirely.

The sizing decision mattered more than the stock pick itself.

Why Equal Weighting Fails (And Why You’re Probably Doing It)

The default position sizing strategy for most investors is equal weighting: divide your portfolio into X positions of roughly equal size.

20 stocks? Each position is ~5%. 30 stocks? Each position is ~3.3%.

Equal weighting feels safe. It feels diversified. It feels like you’re not making any bold bets.

And that’s precisely the problem.

Equal weighting assumes all your investment ideas are equally good.

But you don’t believe that. I know you don’t. You have stocks you’re excited about and stocks you’re “meh” about. You have companies you’d back up the truck for at the right price, and companies you own because they provide exposure to a sector.

Equal weighting ignores these differences entirely. It treats your highest-conviction, lowest-risk ideas the same as everything else in your portfolio.

That’s leaving money on the table.

Framework #1: Conviction-Based Position Sizing

This is where most investors should start: sizing positions based on your confidence in the analysis.

The concept is simple: your position size should reflect your conviction level.

High conviction = larger position

Medium conviction = medium position

Low conviction = smaller position (or no position)

But here’s where it gets practical. You need to define what “high conviction” actually means. Otherwise, everything feels like high conviction when you’re excited about it.

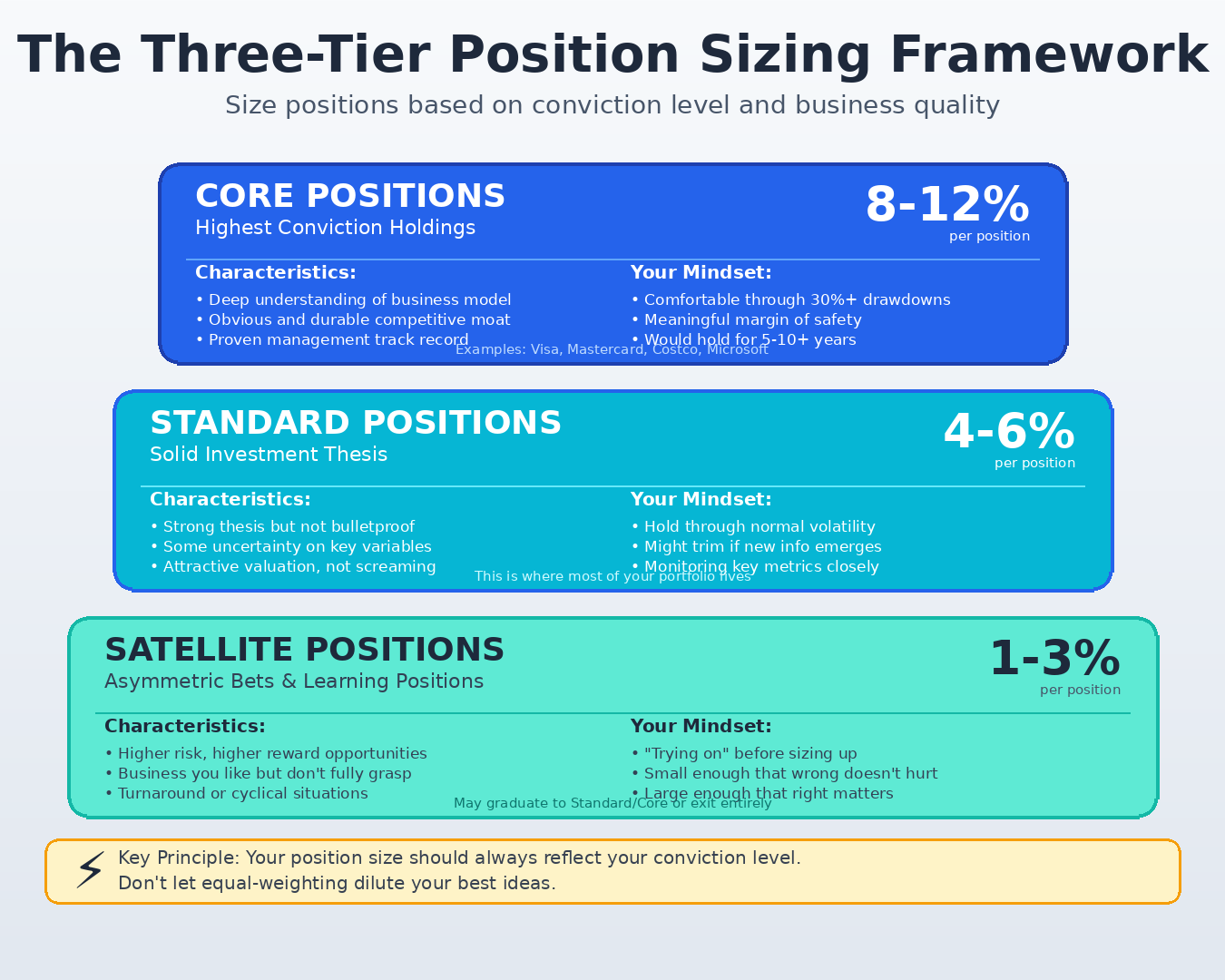

I use a three-tier system:

Core Positions (8-12% each)

These are businesses where:

You understand the business model cold

The competitive moat is obvious and durable

Management has a long track record

The valuation provides a meaningful margin of safety

You’d be comfortable holding through a 30% drawdown

Think: Visa, Mastercard, Costco, Microsoft. Companies where the “what could go wrong” list is short and manageable.

Standard Positions (4-6% each)

These are quality businesses where:

The investment thesis is solid but not bulletproof

There’s some element you’re less certain about (management, competitive dynamics, etc.)

The valuation is attractive but not a screaming bargain

You’d hold through volatility but might trim if new information emerges

Most of your portfolio lives here.

Satellite Positions (1-3% each)

These are:

Higher-risk, higher-reward opportunities

Businesses you like but don’t fully understand yet

Positions you’re “trying on” before potentially sizing up

Turnaround situations or cyclical plays

These are your “asymmetric bets”—small enough that being wrong doesn’t hurt, large enough that being right matters.

Framework #2: Risk-Based Position Sizing

Conviction is critical, but it’s not the whole story.

You also need to account for the position's risk, independent of your conviction level.

This is where business quality and valuation uncertainty come into play.

A simple risk-based framework uses two variables:

Business Quality Score (moat strength, financial health, predictability)

Valuation Uncertainty (how wide is your range of fair value estimates?)

Let me show you how this works in practice:

High Quality + Low Uncertainty = Larger Position

Strong moat, predictable cash flows

Your DCF range is tight (fair value between $180-$200)

Risk Adjustment: Size up by 1-2%

High Quality + High Uncertainty = Standard Position

Strong moat but facing industry headwinds

Your DCF range is wide (fair value between $150-$250)

Risk Adjustment: Keep at base size

Medium Quality + Low Uncertainty = Standard Position

Decent business, some competitive pressure

Your DCF range is reasonably tight

Risk Adjustment: Keep at base size

Medium Quality + High Uncertainty = Smaller Position

Competitive dynamics shifting

Your DCF range is wide OR you’re less confident in assumptions

Risk Adjustment: Size down by 1-2%

The key insight: risk and conviction aren’t the same thing.

You might have high conviction that a turnaround will work (high conviction), but the business itself is risky and your valuation has a wide range (high risk). The conviction suggests a larger position; the risk suggests a smaller one. You need both frameworks working together.

Synthesis: Combining Conviction + Risk

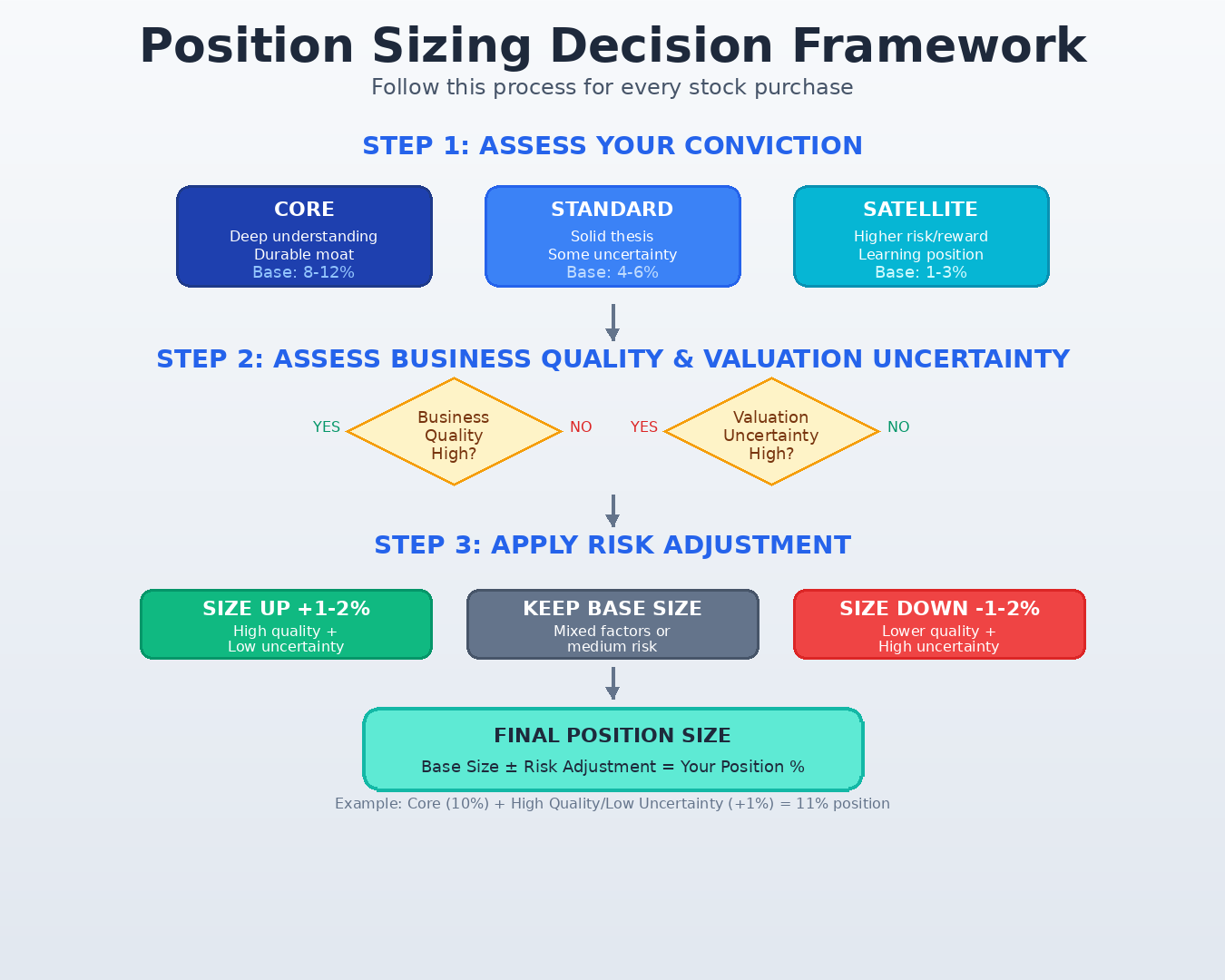

Now let’s put this together into a single decision framework.

Step 1: Determine your conviction tier (Core/Standard/Satellite)

This gives you a base position size range.

Step 2: Assess business quality and valuation uncertainty

This adjusts your position size within that range.

Step 3: Calculate your final position size

Here’s an example:

Company: Applied Materials

Conviction: Core (base range: 8-12%)

Business Quality: High (strong moat, industry leadership)

Valuation Uncertainty: Medium (semiconductor cycles create some variability)

Risk Adjustment: Neutral

Final Position Size: 10%

Company: Regional bank turnaround

Conviction: Standard (base range: 4-6%)

Business Quality: Medium (banking is competitive, integration risks)

Valuation Uncertainty: High (turnaround success is uncertain)

Risk Adjustment: Size down by 1%

Final Position Size: 4%

See how this works? You’re not guessing. You’re making systematic decisions based on clear criteria.

The Counter-Intuitive Strategy: Averaging Up

Here’s where I’ll challenge conventional wisdom.

Most investors average down. They buy a stock at $100, it drops to $80, and they buy more because “it’s cheaper now.”

Sometimes that works. Sometimes it doesn’t.

I prefer averaging up.

Averaging up means buying more of a stock after it’s proven you right. The price has gone up, your thesis is playing out, and you’re adding to a winning position.

Why does this work?

1. You’re reinforcing what’s working

The company is executing. Results are beating expectations. The market is recognizing the value. These are all good signs.

2. You’re limiting damage from being wrong

If your initial thesis was flawed, you find out with a small position. You don’t compound the mistake by averaging down into a deteriorating situation.

3. You’re letting winners run

Many investors trim winners too early. Averaging up keeps you properly sized in your best performers.

Here’s how I implement this:

Start with a 4-5% position (standard size)

If the stock rises 20%+ AND the thesis is strengthening (not just multiple expansion), add another 2-3%

Maximum total position size: 12% for core holdings

Example: You buy Visa at $220 for 5% of your portfolio. Over 12 months, it rises to $280 (up 27%). Revenue growth is accelerating, margins are expanding, and the competitive moat is strengthening. You add another 3%, bringing your total position to 8% of your portfolio (accounting for the gain).

The key is that you’re averaging up based on improving fundamentals, not just price action.

If the stock is up because the P/E expanded from 25 to 35 with no fundamental improvement? Don’t chase it. But if it’s up because the business is crushing it? That’s when you lean in.

Putting It All Together: Your Position Sizing Checklist

Every time you’re ready to buy a stock, run through this checklist:

☐ Conviction Assessment

Do I understand this business model completely?

Is the moat clear and durable?

What’s my confidence level? (Core/Standard/Satellite)

☐ Risk Assessment

How strong is the business quality?

How wide is my fair value range?

Any company-specific risks that increase uncertainty?

☐ Initial Position Size

Base size from conviction tier

Risk adjustment up or down

Final position size: ____%

☐ Averaging Strategy

Am I starting smaller with intent to average up?

Or is this a full position from the start?

What would trigger me to add more?

☐ Portfolio Context

Do I already have similar exposures?

Am I over-concentrated in one sector?

Does this fit my overall portfolio construction?

This systematic approach removes emotion from the decision. You’re not sizing positions based on how excited you feel that day. You’re applying consistent criteria every single time.

Ready to see this framework in action?

The concepts above give you the foundation. But understanding a framework and actually implementing it in your portfolio are two different things.

Below, I walk through:

Real portfolio examples - How I sized positions in TSMC, Visa, and Nubank using this exact framework, including when I added to winners

Advanced considerations - When to break the rules for sector concentration, correlation clustering, and market dislocations

The Position Sizing Audit - A step-by-step process to fix your existing portfolio’s mis-sized positions

Common mistakes - The position sizing errors I see intermediate investors make repeatedly (and how to avoid them)

Your action plan - What to do this weekend to implement this framework in your portfolio

This is where theory becomes practice.