How REITs Work: A Practical Guide for Dividend Investors

What if you could own a piece of a shopping center, a warehouse, or a hospital without ever signing a mortgage or dealing with a tenant? That is exactly what Real Estate Investment Trusts (REITs) offer. They give everyday investors access to commercial real estate through a single stock purchase.

REITs remain one of the most misunderstood corners of the stock market. Many investors skip them entirely because they seem complicated. Others buy them blindly for the dividend yield without understanding the mechanics underneath. Both groups leave money on the table.

In today’s post, we will learn:

• What Is a REIT and How Does It Work?

• The Three Types of REITs

• How REITs Make Money (and Pay You)

• Key Metrics: Why Earnings Per Share Won’t Help You Here

• How to Evaluate a REIT: A Practical Framework

• Investor Takeaway

Okay, let’s dive in and learn more about how REITs work.

What Is a REIT and How Does It Work?

A Real Estate Investment Trust (REIT) is a company that owns, operates, or finances income-producing real estate. Congress created this structure in 1960 to give ordinary investors access to large-scale commercial properties, the same way mutual funds gave them access to diversified stock portfolios.

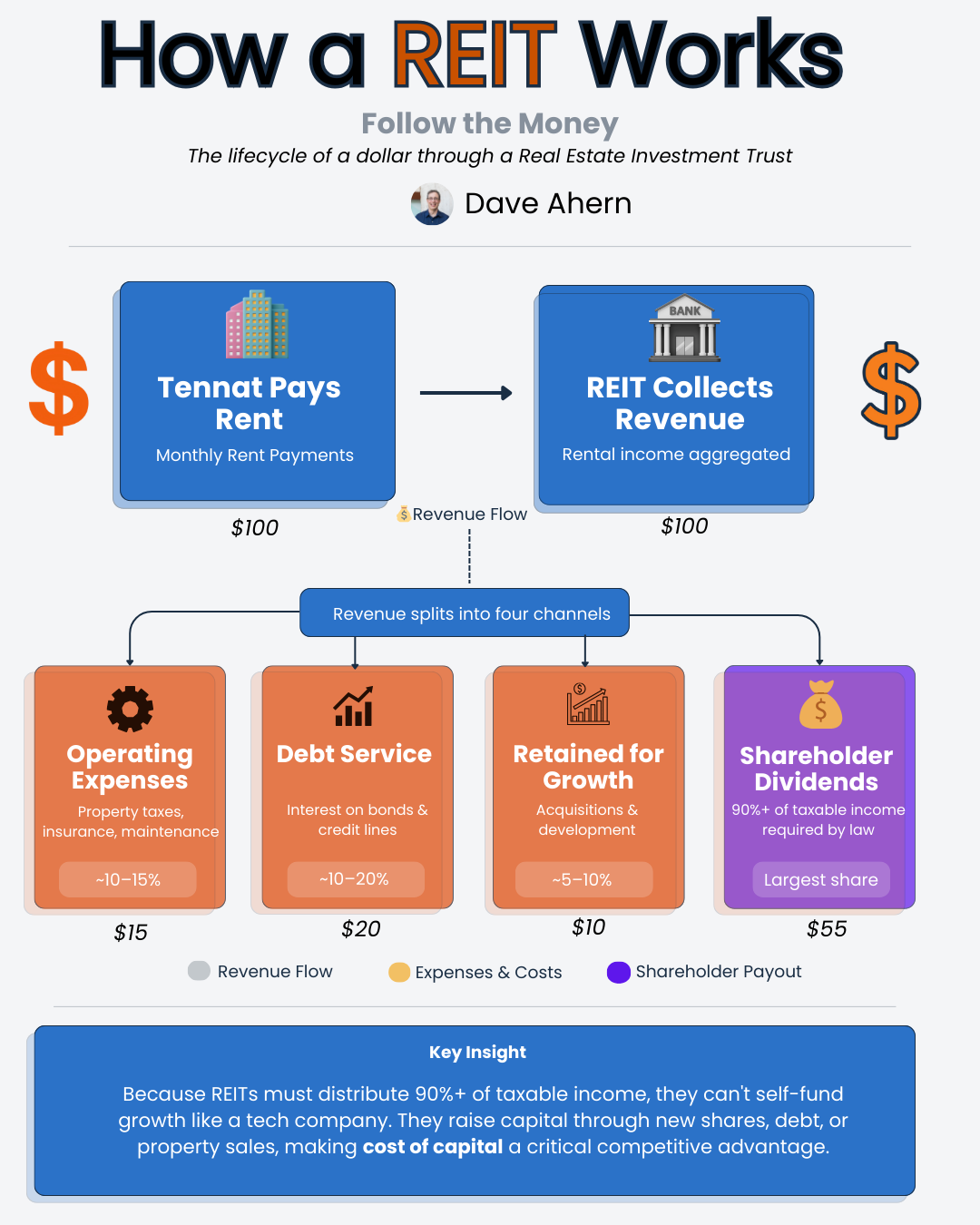

The concept is straightforward. A REIT pools investor capital, buys real estate, collects rent from tenants, and distributes most of that income back to shareholders as dividends. Instead of buying a strip mall yourself, you buy shares in a company that owns hundreds of them.

To qualify as a REIT with the IRS, a company must meet several requirements. The most important ones for investors to understand are:

• Distribute at least 90% of taxable income to shareholders annually as dividends

• Invest at least 75% of total assets in real estate, cash, or U.S. government securities

• Derive at least 75% of gross income from real estate-related sources (rents, mortgage interest, real estate sales)

• Have at least 100 shareholders after its first year

• Have no more than 50% of shares held by five or fewer individuals

That 90% distribution requirement is the big one. It is the reason REITs pay such generous dividends compared to regular corporations. A typical company like Apple or Microsoft can retain all its earnings and reinvest them. A REIT cannot. It must send most of its taxable income out the door to shareholders.

The trade-off? REITs avoid paying corporate-level income tax on the income they distribute. The tax obligation passes to you, the shareholder. This is why REIT dividends are generally taxed as ordinary income rather than at the lower qualified dividend rate. However, investors may deduct up to 20% of qualified REIT dividends through the Section 199A qualified business income deduction, which helps offset that higher tax rate.

Think of a REIT as a pipeline. Rent flows in from tenants, passes through the company (minus operating expenses), and flows out to you as dividends. The company keeps just enough to maintain and grow the portfolio.

The Three Types of REITs

Not all REITs are created equal. They come in three broad categories, and understanding the differences matters for your portfolio.

Equity REITs

Equity REITs own and operate income-producing real estate. They collect rent from tenants, maintain properties, and benefit from property appreciation over time. This is the most common type, representing the vast majority of publicly traded REITs.

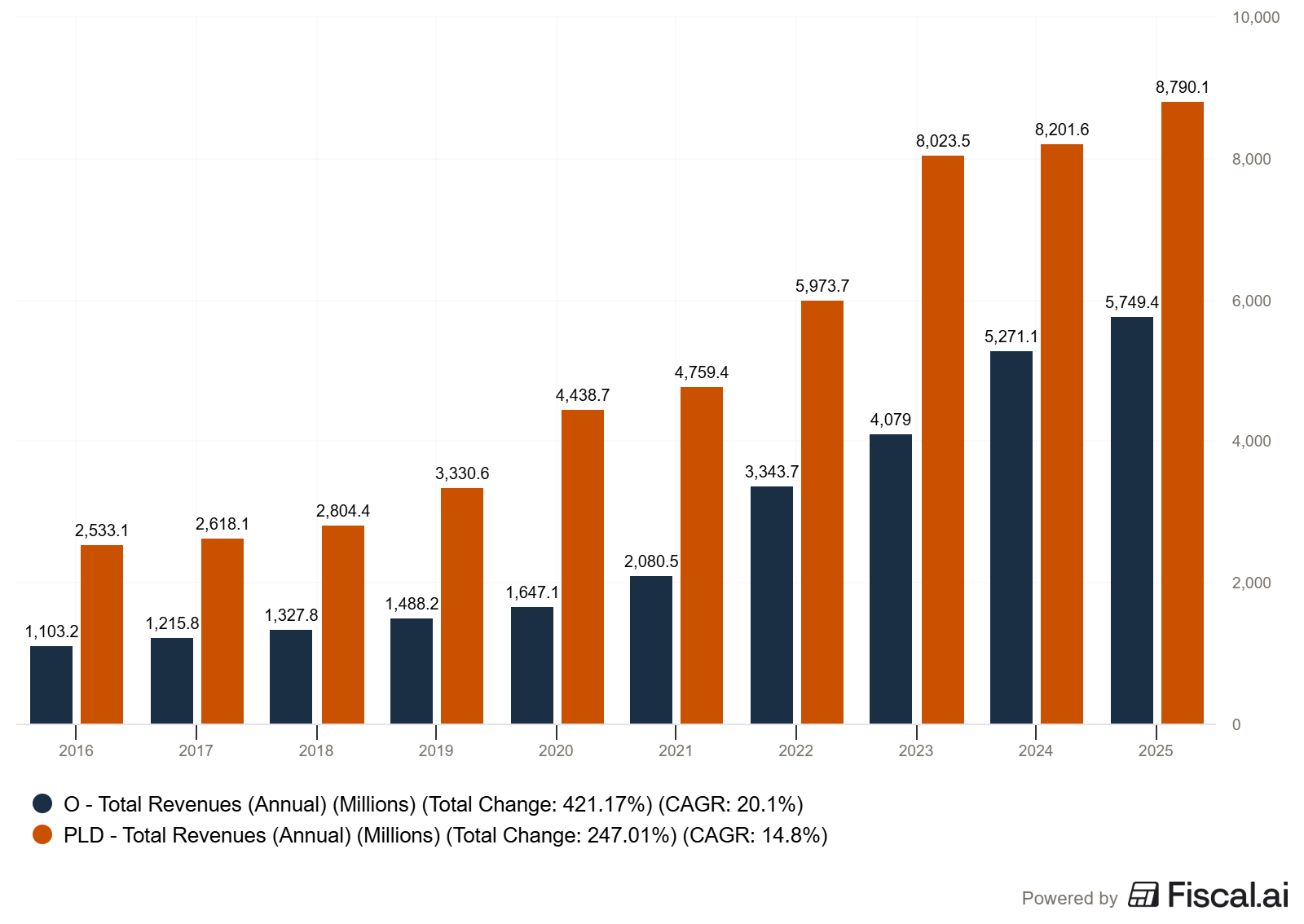

Realty Income (ticker: O) is the textbook example. The company owns over 15,450 properties across all 50 U.S. states, plus the U.K. and six other European countries. Its tenants include names you recognize: Walgreens, Dollar General, FedEx, and Walmart. When those tenants pay rent each month, Realty Income collects that income and distributes it to shareholders. The company has earned the nickname “The Monthly Dividend Company” because it pays dividends every month rather than quarterly.

Prologis (ticker: PLD) offers another angle. Instead of retail storefronts, Prologis owns logistics warehouses. With approximately 1.2 billion square feet across 20 countries and roughly 6,500 customers, Prologis sits at the center of global e-commerce. Every package Amazon delivers likely passed through a Prologis warehouse at some point.

Mortgage REITs (mREITs)

Mortgage REITs don’t own physical properties. Instead, they lend money to real estate owners or invest in mortgage-backed securities. They profit from the spread between the interest they earn on mortgage loans and the cost of their own borrowing.

Annaly Capital Management (NLY) is one of the largest mREITs. These are fundamentally different businesses from equity REITs. They behave more like financial institutions than property companies. They carry a higher risk because they are sensitive to interest rate changes, and their dividends can be volatile. For most dividend-focused investors, equity REITs will be the better fit.

Hybrid REITs

Hybrid REITs combine both approaches, owning properties and holding mortgages. They are less common and tend to be more complex. For simplicity, we will focus the rest of this article on equity REITs, which are the bread and butter of most REIT investors.

Knowing the concepts is one thing. Being able to sit down with a real dividend stock and actually analyze it is another. Paid membership gives you the tools to bridge that gap:

📊 1. Stock Analysis Infographic Library: 180+ visual references covering financial statements, valuation multiples, and dividend metrics, your cheat sheet for analyzing any company

🤖 2. AI Prompt Library: 10 purpose-built prompts that turn AI into a research partner, stress-test your thesis, dig into financials faster, and catch risks you’d otherwise miss

🔧 3. Investing Tools Suite: 4 analytical tools that take the friction out of the numbers so you can focus on understanding the business, not wrestling with spreadsheets

🎓 4. Skill Workshop: Practical working sessions walking through real company analysis start to finish, not theory, not lectures, actual practice

📈 5. Dividend Analysis Course (Coming Soon): A complete step-by-step course on analyzing dividend stocks using Buffett-inspired fundamental analysis

🔓 6. Everything Added Going Forward: Every new resource, tool, and prompts added automatically, no extra charge, ever

How REITs Make Money (and Pay You)

The revenue model for an equity REIT comes down to one thing: rent. But the details of how that rent flows matter for evaluating quality.

Most commercial REITs use long-term lease agreements with tenants. Realty Income, for example, primarily uses net lease structures. Under a net lease, the tenant pays the base rent plus most or all of the property’s operating expenses: property taxes, insurance, and maintenance. This shifts the cost burden from the REIT to the tenant, creating a more predictable income stream for the REIT and its shareholders.

The beauty of this structure is its simplicity. The REIT collects rent. It pays its own corporate expenses, debt service, and any property costs not covered by tenants. What remains gets distributed to shareholders.

REITs grow their income through three primary channels:

• Rent escalations: Most leases include built-in rent increases, either fixed annual bumps (often 1% to 3%) or tied to inflation. This provides organic growth without any additional capital investment.

• Acquisitions: REITs buy additional properties to expand their portfolio. Realty Income invested $1.72 billion in 308 properties during Q4 2024 alone. This is a primary growth lever for large REITs.

• Development: Some REITs, like Prologis, build new properties from the ground up. Prologis generated $773 million in value creation from development stabilizations in 2024. Development offers higher returns but carries more risk than buying existing properties.

Here is where the 90% distribution rule creates a unique challenge. Because REITs must pay out most of their income, they can’t self-fund growth the way a tech company can. To acquire or develop new properties, REITs typically raise capital through three methods: issuing new shares (equity), taking on debt (bonds or credit lines), or selling existing properties to redeploy capital.

This means the cost of capital matters enormously for REITs. A REIT that can borrow cheaply and issue shares at a premium to asset value has a significant advantage over competitors. It can grow without destroying value for existing shareholders.

Key Metrics: Why Earnings Per Share Won’t Help You Here

This is where many investors trip up. If you try to analyze a REIT using the same metrics you use for Apple or Microsoft, you will get misleading results.

The problem starts with net income. REITs own physical buildings, and accounting rules require them to depreciate those buildings over time. A warehouse bought for $50 million gets written down a little each year on the income statement, reducing reported earnings. But here is the thing: real estate doesn’t lose value the way a computer or a piece of factory equipment does. In many cases, the property appreciates over time.

This depreciation expense makes net income artificially low for REITs, which makes traditional metrics like P/E ratio unreliable. That is why the REIT industry developed its own set of metrics.

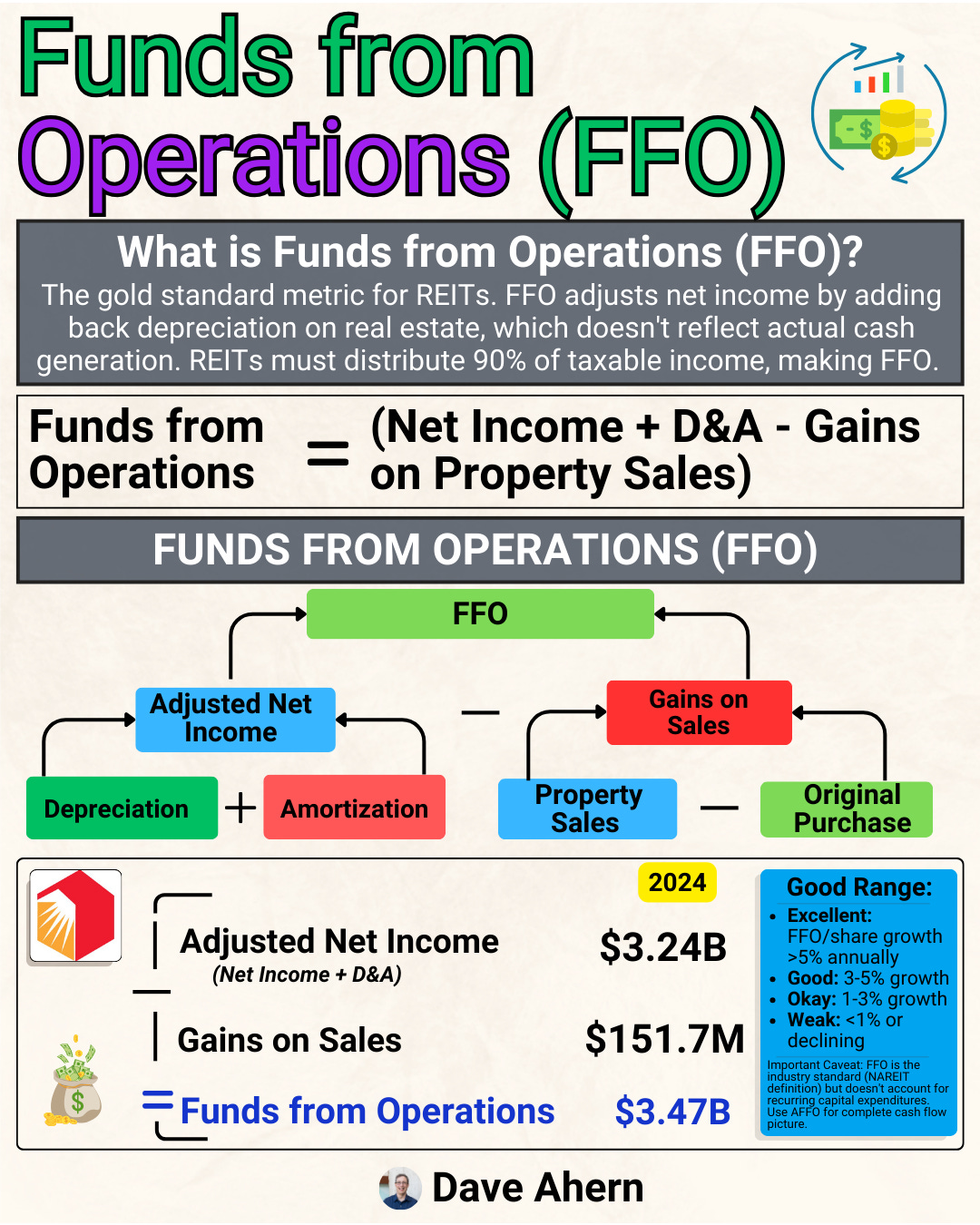

Funds From Operations (FFO)

Funds From Operations (FFO) is the REIT equivalent of earnings per share. The National Association of Real Estate Investment Trusts (Nareit) defines FFO as net income plus depreciation and amortization of real estate assets, plus impairment charges on depreciable real estate, minus gains on property sales.

In simple terms, FFO adds back the depreciation that artificially reduced net income and removes one-time gains from selling properties. This gives you a cleaner picture of the REIT’s recurring operating performance.

Prologis reported Core FFO of $5.56 per share for fiscal year 2024, while net earnings came in at $4.01 per share. That $1.55 gap is almost entirely explained by depreciation. If you valued Prologis on net earnings alone, you would significantly undervalue the company.

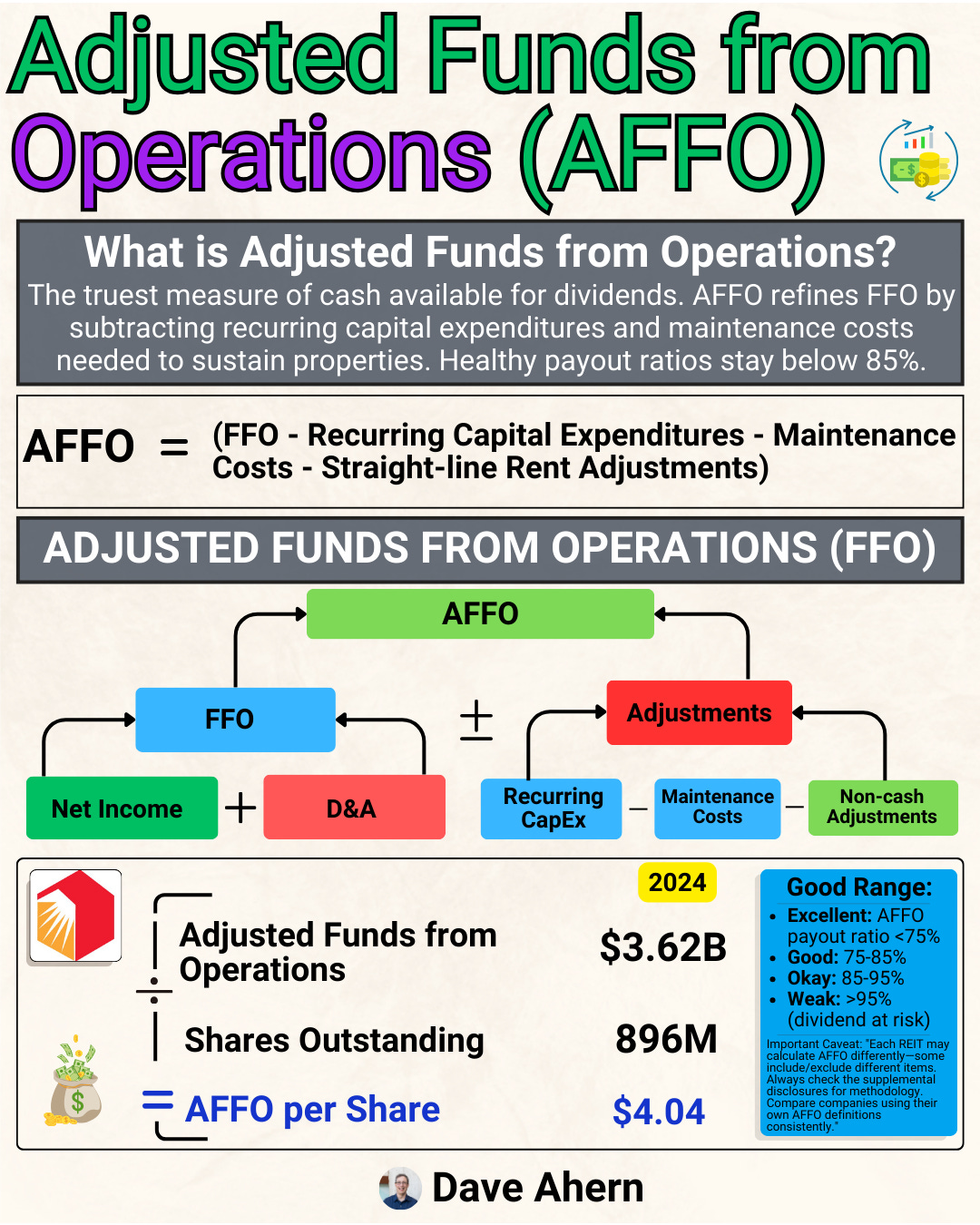

Adjusted Funds From Operations (AFFO)

AFFO takes FFO one step further. It adjusts for recurring capital expenditures (the money a REIT must spend to maintain its properties), straight-line rent adjustments, and other non-cash items. Think of AFFO as the truest measure of how much cash a REIT can actually distribute to shareholders.

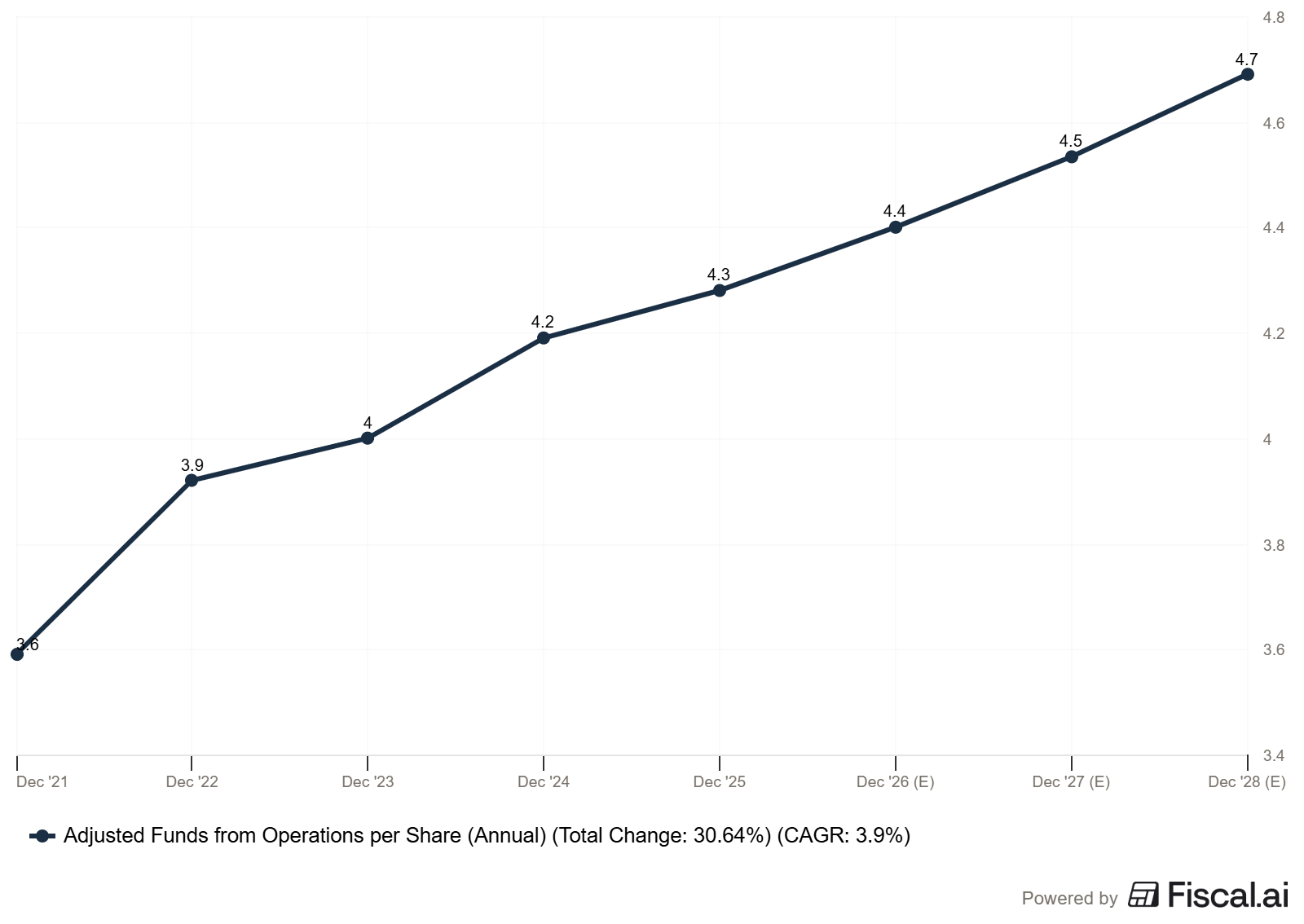

Realty Income reported AFFO of $4.19 per share for fiscal year 2024, representing its 14th consecutive year of annual AFFO per share growth. With an annualized dividend of approximately $3.16 per share (as of year-end 2024), the company’s AFFO payout ratio came to roughly 75%. That leaves a comfortable cushion to cover unexpected expenses and fund modest growth.

A quick note: not all REITs calculate FFO and AFFO the same way, so direct comparisons between companies require looking at what each includes and excludes. Always check the reconciliation table in the company’s earnings release, which shows how they bridge from net income to FFO to AFFO.

Other Key Metrics

Beyond FFO and AFFO, here are the metrics I look at when evaluating a REIT:

• Occupancy rate: What percentage of the REIT’s properties are leased? Realty Income maintained 98.7% occupancy as of December 31, 2024. Higher occupancy means more stable rent collection. I like to see occupancy above 95% for established REITs.

• Net debt to EBITDA: This measures how many years it would take the REIT to pay off its debt using operating income. Lower is better. A ratio above 6x to 7x starts to signal elevated risk.

• Dividend payout ratio (AFFO basis): What percentage of AFFO goes to dividends? A ratio between 70% and 85% is generally healthy. Too low might mean the REIT isn’t returning enough to shareholders. Too high (above 90%) leaves little room for error.

• Same-store rent growth: Are rents increasing on properties the REIT has owned for at least a year? This isolates organic growth from acquisition-driven growth.

How to Evaluate a REIT: A Practical Framework

Now that we understand the mechanics, let’s put together a practical framework you can use to evaluate any REIT. I think of it as five questions.

1. Do I Understand the Property Type?

REITs span dozens of property types: retail, industrial, office, healthcare, data centers, cell towers, self-storage, timber, and more. Stick with what you understand. If you can explain why tenants need the space and why they would have trouble leaving, you are off to a good start.

Warren Buffett’s first filter applies here: invest in businesses you can understand. A net-lease retail REIT is straightforward. A mortgage REIT using complex derivatives is not.

2. Is the Dividend Sustainable?

Check the AFFO payout ratio. If the REIT pays out 95% or more of its AFFO, the dividend has little margin of safety. Look at the trend over three to five years. Is AFFO per share growing or shrinking? Realty Income’s track record speaks volumes: 14 consecutive years of AFFO per share growth and 109 consecutive quarterly dividend increases as of December 2024.

3. How Strong Is the Balance Sheet?

Debt matters more for REITs than for most companies because REITs rely on external capital to grow. Check the credit rating (investment-grade is preferred), the net debt-to-EBITDA ratio, and the debt maturity schedule. A REIT with a wall of debt maturing in a high-interest-rate environment faces real risk.

4. What Are the Growth Prospects?

Growth in the REIT world comes from rent escalations, acquisitions, and development. Look at the embedded rent growth in existing leases, the pipeline of acquisitions, and management’s track record of deploying capital at attractive spreads. Realty Income’s Q4 2024 investments came at an initial weighted average cash yield that exceeded its cost of capital, a sign of disciplined capital allocation.

5. Am I Paying a Fair Price?

The most common valuation metric for REITs is the Price-to-FFO ratio, which functions like a P/E ratio for regular stocks. Compare the current P/FFO to the REIT’s historical average and to sector peers. You can also look at the dividend yield relative to its historical range, though yield alone should never be your sole valuation tool.

A high dividend yield can be a sign of a bargain, or it can be a warning that the market expects a dividend cut. Context matters.

Common Mistakes REIT Investors Make

Before we wrap up, let me flag a few pitfalls I see regularly.

Chasing yield is the biggest one. A REIT yielding 10% when its peers yield 4% is not a bargain. It is usually a signal that the market expects trouble. The dividend may be at risk of a cut, or the underlying properties may be deteriorating.

Using the P/E ratio instead of the P/FFO is another common error. As we discussed, depreciation makes net income unreliable for REITs. If you screen REITs by P/E, you will filter out quality companies that look “expensive” only because of accounting conventions.

Ignoring the balance sheet is the third mistake. Some investors focus only on the dividend and never check the debt levels. REITs that over-leverage to juice returns can face serious trouble when interest rates rise or credit markets tighten. The pandemic taught this lesson to several office and retail REITs.

Finally, treating all REITs the same will lead you astray. An industrial warehouse REIT and a regional mall REIT operate in completely different economic realities. Always evaluate REITs within their specific property sector.

Investor Takeaway

REITs offer investors something unique: access to large-scale commercial real estate with the liquidity of a stock and the income of a landlord. The 90% distribution requirement means REITs are built to pay dividends, making them natural fits for income-focused portfolios.

But the same rules that make REITs great dividend payers also make them capital-dependent. Understanding how a REIT funds its growth, evaluating the sustainability of its dividend through AFFO, and checking the balance sheet are all essential steps before investing.

The framework is simple. Understand the property type. Verify the dividend is covered by AFFO. Check the debt. Assess growth prospects. Pay a fair price. If you can check those five boxes, you are well on your way to building a quality REIT position in your portfolio.

That will wrap up our discussion for today.

As always, thank you for taking the time to read this post, and I hope you find something of value on your investing journey.

If I can further assist, please don’t hesitate to reach out.

Until next time, take care and be safe out there,

Dave

Knowing the concepts is one thing. Being able to sit down with a real dividend stock and actually analyze it is another. Paid membership gives you the tools to bridge that gap:

📊 1. Stock Analysis Infographic Library: 180+ visual references covering financial statements, valuation multiples, and dividend metrics, your cheat sheet for analyzing any company

🤖 2. AI Prompt Library: 10 purpose-built prompts that turn AI into a research partner, stress-test your thesis, dig into financials faster, and catch risks you’d otherwise miss

🔧 3. Investing Tools Suite: 4 analytical tools that take the friction out of the numbers so you can focus on understanding the business, not wrestling with spreadsheets

🎓 4. Skill Workshop: Practical working sessions walking through real company analysis start to finish, not theory, not lectures, actual practice

📈 5. Dividend Analysis Course (Coming Soon): A complete step-by-step course on analyzing dividend stocks using Buffett-inspired fundamental analysis

🔓 6. Everything Added Going Forward: Every new resource, tool, and prompts added automatically, no extra charge, ever

Most people will scroll past this and keep trying to ‘pick winners’ instead of building income streams. That’s the real gap.

Wow🤗🤗🇿🇦🇿🇦🇿🇦🫡🫡🫡🫡💫You have answered my one of my prayers.www.insephe.co.za.

I personally Thank you.you Read my vision or responded.As A President of My Own Yound Old Youth of the Globe🫡🫡🫡🫡🫡🫡🫡🇿🇦🇿🇦⚓️⚓️⚓️💫🌻🌻🌻🌻.