How Danaher Executes: Three Advantages That Built a $160 Billion Life Sciences Powerhouse

When most investors think about quality niches, they picture obvious moats like network effects or brand power. But some of the best long-term compounders operate in less glamorous spaces where execution matters more than the spotlight.

Life sciences instrumentation is one such niche.

The companies that sell lab equipment, consumables, and diagnostic tools to researchers and hospitals don’t make headlines. But they generate extraordinary returns when executed well. Danaher (NYSE: DHR) proves the point. Over the past 40 years, they’ve compounded shareholder value at roughly 20% annually by systematically winning in this niche.

The promise: This article shows you how Danaher executes in life sciences instrumentation. You’ll learn the three structural advantages they’ve built (most companies have none), how they show up in the numbers, and what to look for when evaluating similar companies in this space.

Why Life Sciences Instrumentation Works as a Niche

Before diving into Danaher’s execution, understand what makes this niche attractive. Life sciences instrumentation has five characteristics that create sustainable competitive advantages:

Mission-critical products. Labs can’t function without their instruments. When Beckman Coulter ships a flow cytometer to a pharmaceutical company’s research facility, that machine becomes embedded in their drug development workflow. Switching costs aren’t just financial. They’re operational and regulatory.

Recurring revenue through consumables. The razor-and-blades model works perfectly here. According to Danaher’s 2024 10-K, their businesses are “typically characterized by a high level of products and services that are sold on a recurring basis.” Once installed, instruments require ongoing purchases of reagents, filters, calibration kits, and service contracts. This creates annuity-like revenue streams.

High switching costs. Validating a new instrument in a regulated environment (think FDA-approved diagnostic labs) costs time and money. Labs standardize on specific platforms and train technicians on them. Switching vendors means revalidation, retraining, and workflow disruption.

Fragmented customer base. No single customer dominates. Danaher sells to pharmaceutical companies, biotech startups, academic institutions, hospitals, and reference labs worldwide.

In 2024, roughly 43% of their revenue came from North America, 23% from Western Europe, and 29% from high-growth markets like China. Geographic and customer diversification smooths volatility.

Long product lifecycles with innovation cycles. Instruments last years. Upgrades happen gradually. This creates predictable replacement cycles and gives strong operators time to build relationships and extract maximum lifetime value from each customer.

The niche works. But execution determines who wins. Danaher has executed better than anyone.

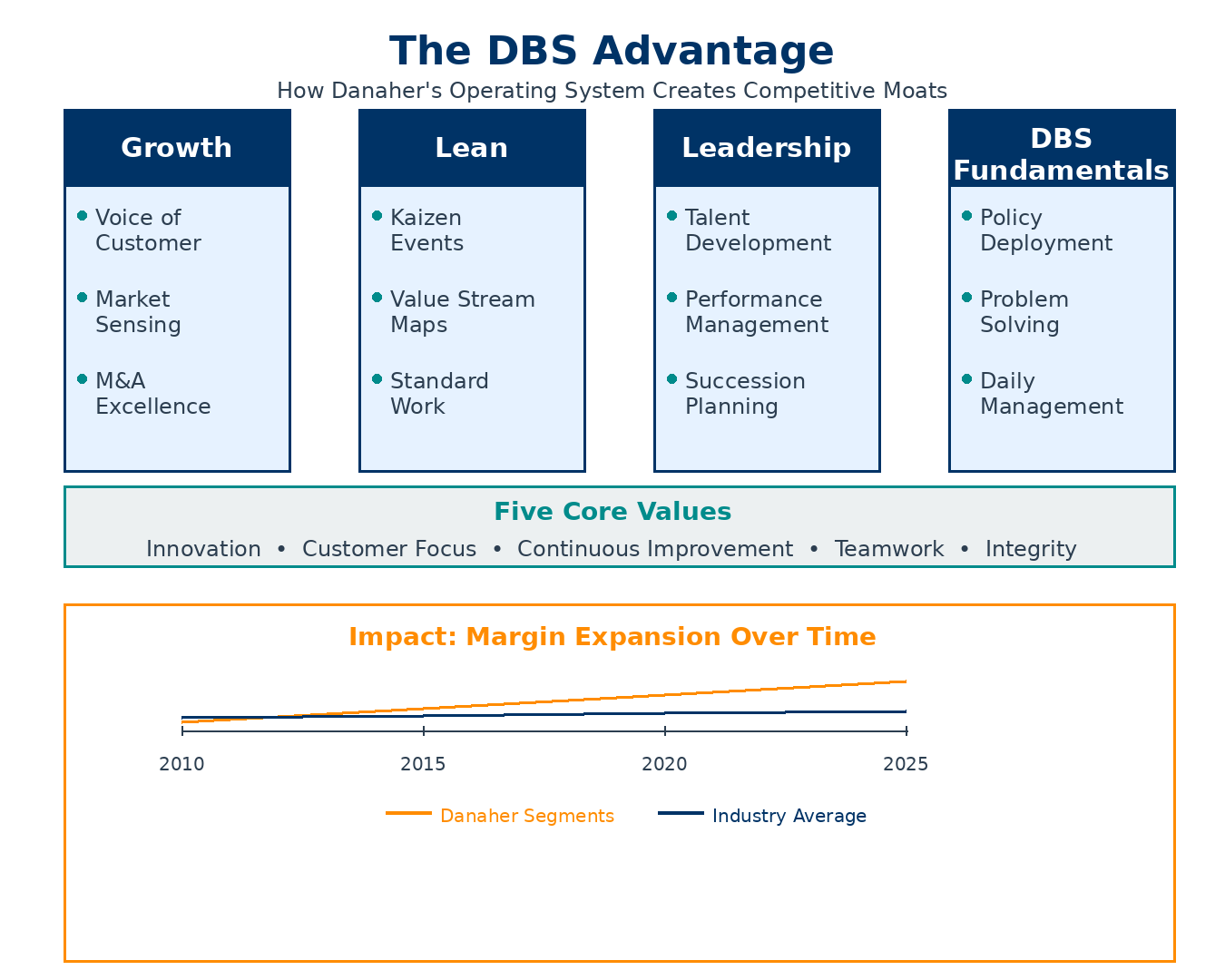

Advantage 1: The Danaher Business System (DBS)

Danaher doesn’t just buy good businesses. They systematically make them better using DBS, their proprietary operating system. Most conglomerates talk about operational excellence. Danaher actually delivers it.

What DBS actually is. DBS is both a toolkit and a culture. According to the 10-K, it’s organized around four pillars:

Growth (expanding markets and customer relationships)

Lean (eliminating waste and improving processes)

Leadership (developing talent systematically)

DBS Fundamentals (daily management and problem-solving)

The system stems from five core values: The Best Team Wins, Customers Talk We Listen, Innovation Defines Our Future, Continuous Improvement Drives Everything, and The Power of Simplicity. These aren’t platitudes. They’re embedded in how every acquired company operates post-acquisition.

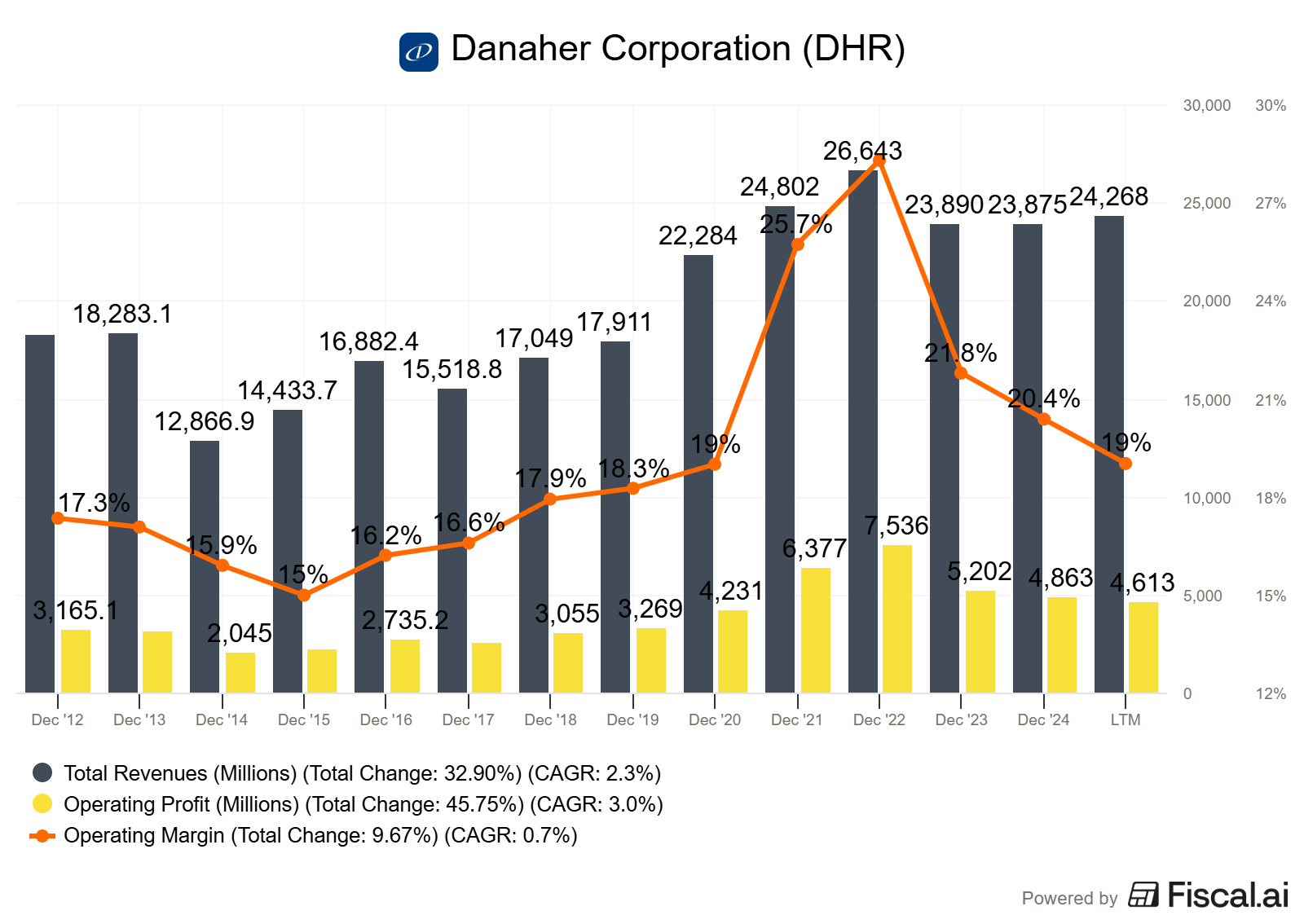

How it shows up in the margins. Look at Danaher’s segment-level operating margins from their 2024 10-K:

Total 2024: $23,875M in revenue with strong segment-level profitability.

These margins exist because DBS drives operational efficiency across the portfolio. The Diagnostics segment, for example, maintained an operating margin of 26.8% in 2024 despite serving cost-conscious hospital systems. That margin doesn’t happen by accident. It happens through relentless process improvement, waste elimination, and value engineering.

The Life Sciences segment’s lower 12.0% margin reflects a different business mix (more instruments, fewer consumables), but even here, DBS creates an advantage. When Danaher acquired Abcam in 2023, it immediately began applying DBS tools to improve manufacturing efficiency and customer service. These gains compound over time.

Continuous improvement as a competitive moat. Most companies improve in spurts. Danaher improves continuously. Every operating company runs daily huddles, tracks key performance indicators, and uses kaizen events to solve problems at the source. This creates a compounding advantage. Competitors need to not just catch up to where Danaher is today, but where they’ll be tomorrow after another cycle of improvement.

The 10-K states it plainly: DBS is “not only the set of business processes and tools our operating companies use on a daily basis in the pursuit of continuous improvement, but also represents our culture.”

Above, we covered why life sciences instrumentation is a niche and how Danaher's operating system (DBS) creates competitive advantages that translate into segment margins of 24.9% to 26.8%.

Below, I'll show you how their M&A machine systematically builds portfolio value (most serial acquirers destroy it), how their recurring revenue model creates cash-flow stability, and the specific metrics you should use to screen for when evaluating similar companies in this space.