How Applied Materials (AMAT) Makes Money

Understanding the semiconductor industry remains essential for investors looking to capitalize on the technology revolution. While many investors focus on chip designers like NVIDIA or manufacturers like Intel, there’s another critical player in this ecosystem that often gets overlooked: the companies that make the equipment used to manufacture semiconductors.

Applied Materials sits at the heart of the semiconductor supply chain, and understanding how this company makes money can help you make better portfolio construction decisions and identify investment opportunities beyond the headline-grabbing chip companies.

Okay, let’s dive in and learn more about how Applied Materials makes money.

What is Applied Materials?

Before we dig into the business model, let’s establish what Applied Materials actually does.

According to their fiscal 2024 10-K filing, Applied Materials provides “manufacturing equipment, services, and software to the semiconductor, display, and related industries.” The company operates through three main segments: Semiconductor Systems, Applied Global Services, and Display and Adjacent Markets.

Here’s the crucial distinction that many investors miss: Applied Materials doesn’t make semiconductors—they make the equipment that makes semiconductors. Think of them as the company that sells the shovels during a gold rush, rather than the company mining for gold.

This positioning matters a great deal for investors. While chip companies like NVIDIA design chips and foundries like TSMC manufacture them, Applied Materials provides the tools and equipment that enable the manufacturing process. This gives them a unique business model with different dynamics, risks, and opportunities than the chip makers themselves.

Not too hard, was it?

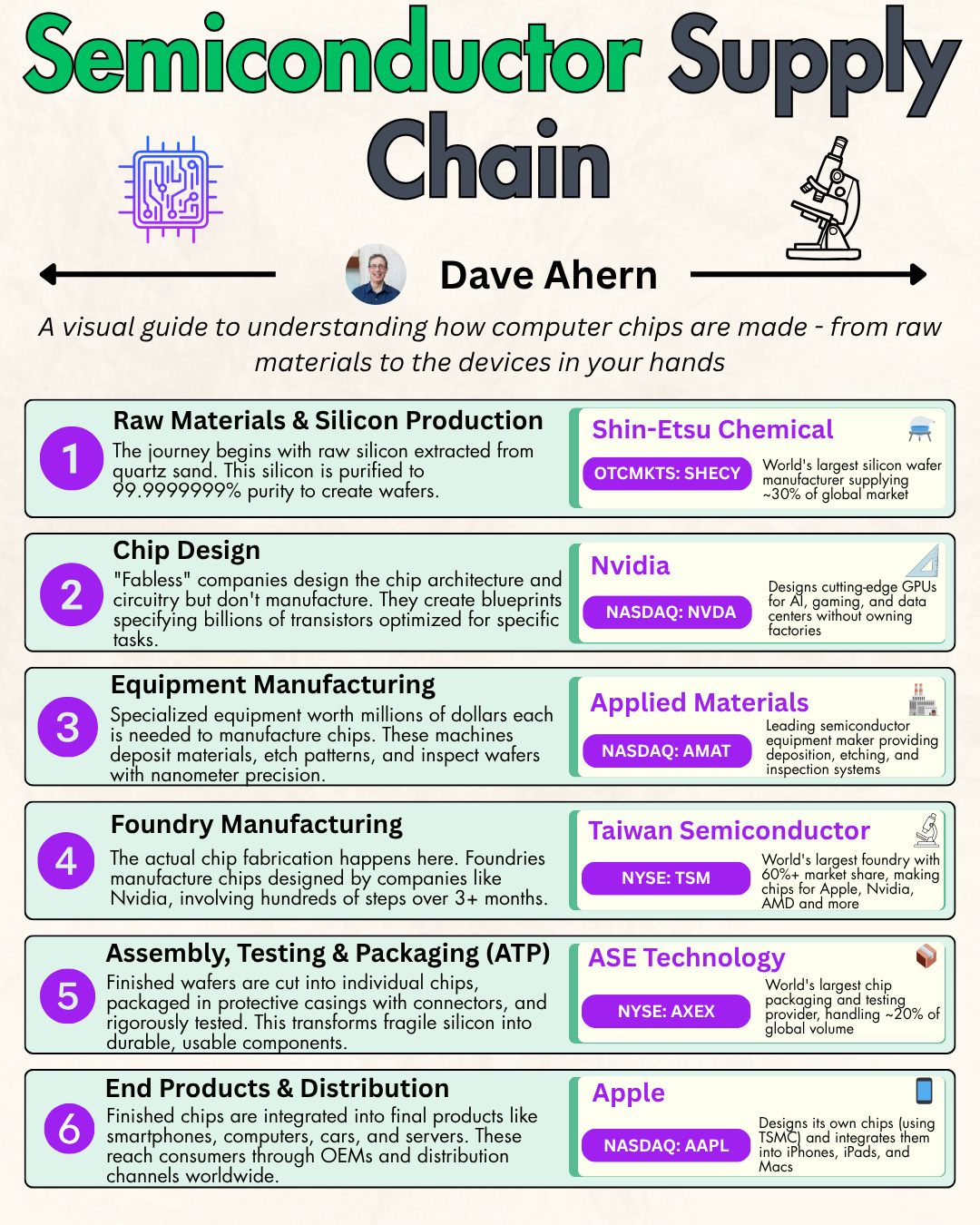

Understanding the Semiconductor Supply Chain

I know it looks scary when you first encounter terms like “fab-less,” “foundry,” and “equipment maker,” but understanding these distinctions remains critical for semiconductor investors.

Let’s break down the key players in the semiconductor supply chain:

Fab-less Chip Designers (like NVIDIA):

Design semiconductor chips

Do not manufacture chips themselves

Outsource production to foundries

Focus on intellectual property and chip architecture

Example: NVIDIA designs GPUs for AI and gaming

Foundries (like TSMC, Samsung, Intel):

Manufacture semiconductor chips for others (or themselves)

Own and operate fabrication facilities (”fabs”)

Require massive capital investment in equipment

Customers include fab-less chip designers

Equipment Makers (like Applied Materials):

Design and sell the equipment that foundries use

Provide the tools for deposition, etching, inspection, and other manufacturing processes

Also provide ongoing service and support

Customers are the foundries and integrated manufacturers

The supply chain flows like this: Chip Designers → Equipment Makers → Foundries → End Products

Here’s where it gets interesting for investors: when NVIDIA’s chip demand explodes due to AI, foundries like TSMC need to expand capacity. To expand capacity, they need to buy equipment from Applied Materials. This means that Applied Materials benefits from the same trends driving chip demand, but at a different point in the value chain.

Remember that each of these business models operates with different economics, margins, capital requirements, and risk profiles.

A fab-less company like NVIDIA has high margins and low capital requirements. A foundry has lower margins and massive capital requirements. An equipment maker like Applied Materials sits in between, with solid margins and recurring service revenue.

Applied Materials’ Business Segments

Now that we understand where Applied Materials sits in the supply chain, let’s examine how they generate revenue. The company operates through three main business segments.

According to their fiscal 2024 financial statements, here’s how Applied Materials breaks down their business:

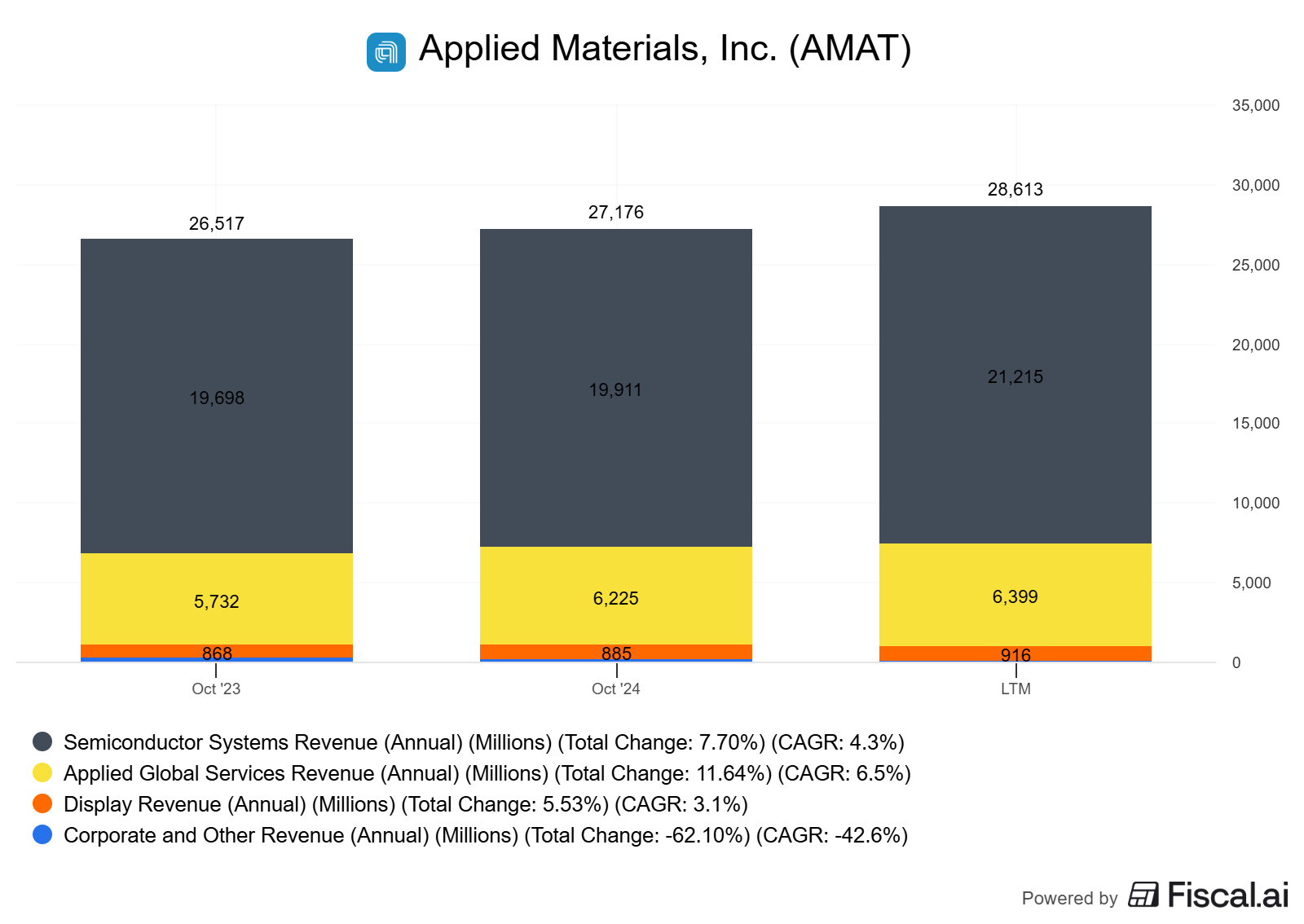

1. Semiconductor Systems (73.7% of revenue)

This segment remains Applied Materials’ largest and most important business. The Semiconductor Systems group develops, manufactures, and sells equipment used to fabricate semiconductor chips.

The equipment in this segment performs critical manufacturing processes:

Deposition: Adding thin layers of materials onto silicon wafers

Etching: Selectively removing materials to create patterns

Ion Implantation: Modifying electrical properties of materials

Inspection and Metrology: Measuring and verifying chip features

Chemical Mechanical Planarization (CMP): Smoothing wafer surfaces

These aren’t simple machines. Each system can cost millions of dollars and represents years of research and development. More importantly, as chips become more complex (think: AI chips, advanced processors), the equipment needs to become more sophisticated, which expands Applied Materials’ addressable market.

2. Applied Global Services (23.0% of revenue)

This segment provides the recurring revenue that makes Applied Materials’ business model so attractive. The Applied Global Services group offers:

Spare parts for installed equipment

Equipment upgrades and retrofits

Maintenance and repair services

Training and support

Software solutions for fab optimization

This matters because once a foundry buys Applied Materials equipment, it needs ongoing support to keep it running. This creates a long-term relationship and a predictable revenue stream.

Think of it like selling a printer and then selling ink cartridges—except the “ink” in this case is highly specialized spare parts and services that keep multi-million-dollar equipment operational.

3. Display and Adjacent Markets (3.3% of revenue)

This smaller segment provides equipment for manufacturing displays (TVs, smartphones, monitors) and other applications like solar panels. While less significant to the overall business, it provides some diversification beyond semiconductors.

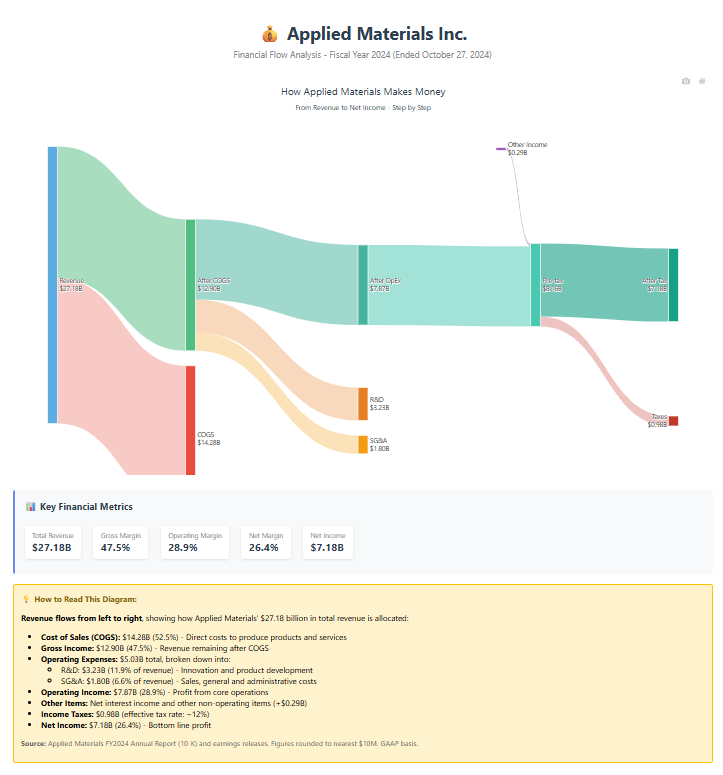

How Applied Materials Generates Revenue

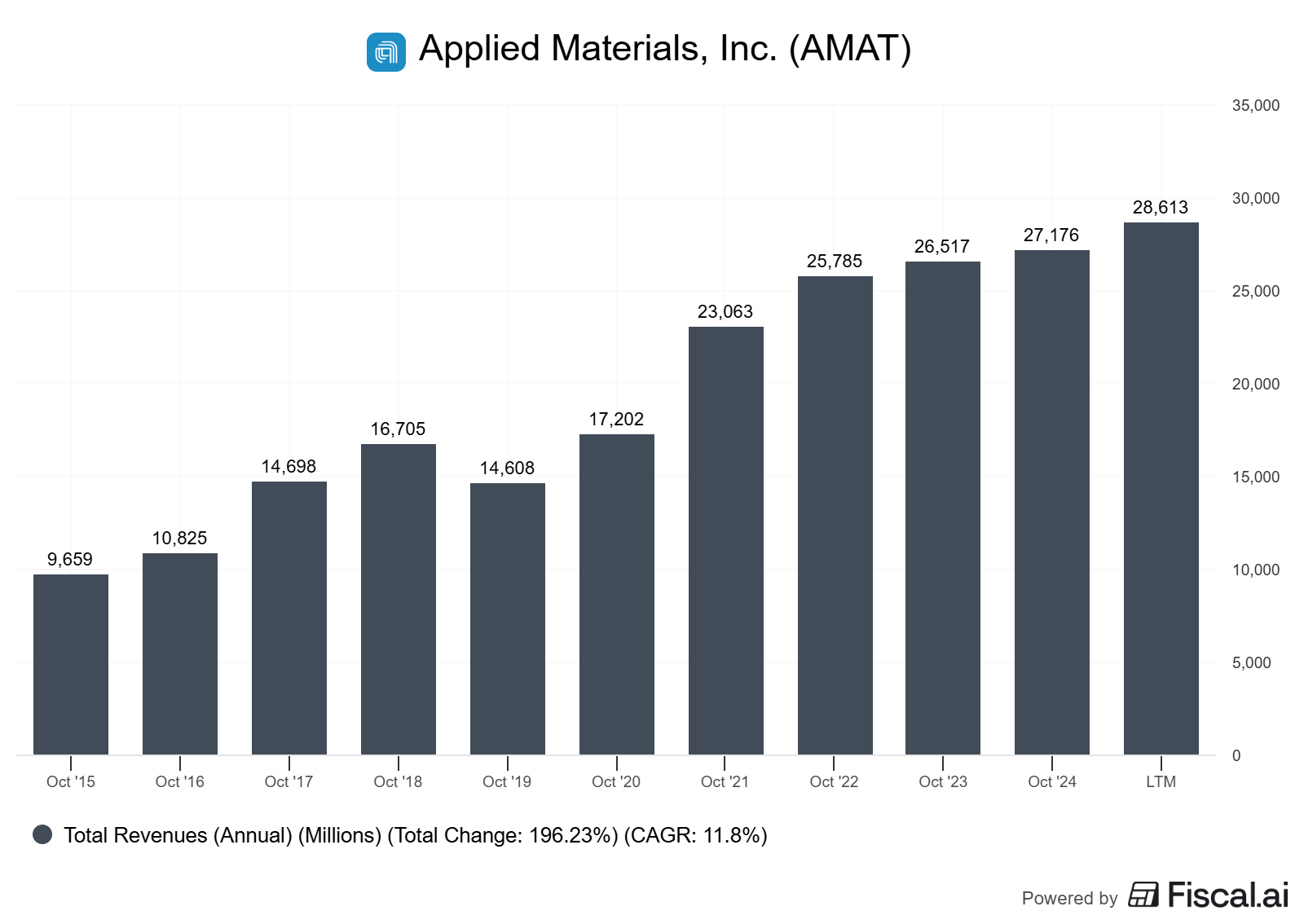

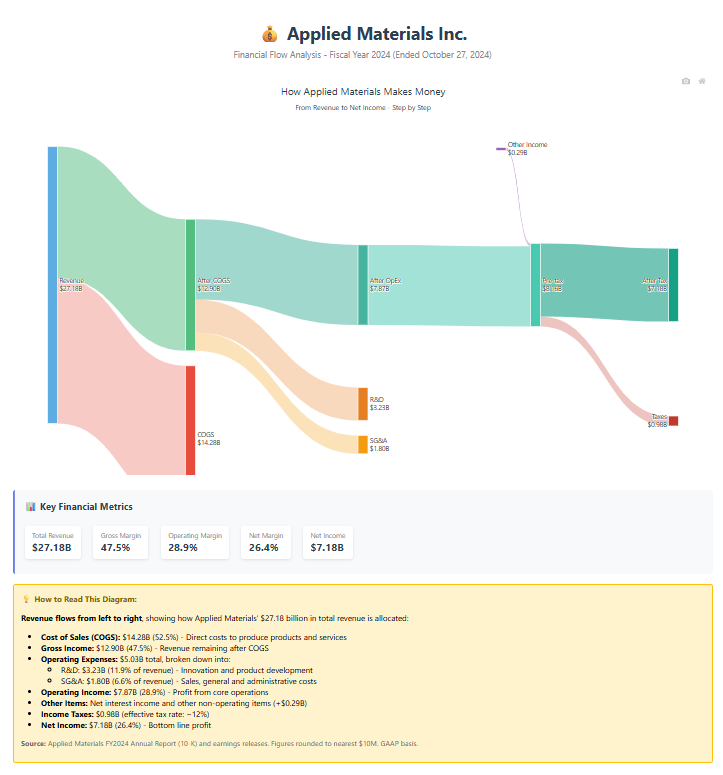

Let’s look at the actual numbers to see how Applied Materials makes money. Using data from their fiscal 2024 10-K, we can build a complete picture of their revenue generation.

Several patterns emerge from this data:

1. Semiconductor Systems Growth Remains Modest

The core equipment business grew just 4.3% over three years. This reflects the cyclical nature of semiconductor equipment spending. Foundries don’t buy new equipment every year—they make large capital investments during expansion cycles and then moderate spending during slower periods.

However, the absolute revenue remains substantial at nearly $20 billion annually. This reflects Applied Materials’ dominant position in the equipment market.

2. Services Revenue Shows Steady Growth

The Applied Global Services segment grew 6.5% over the three-year period, outpacing the equipment segment. This demonstrates the value of the recurring revenue model. Even when equipment sales slow, the installed base continues generating service revenue.

In fiscal 2024, services accounted for 23% of total revenue. This provides stability during industry downturns and generates higher margins than equipment sales.

3. Display Business Contracted

The Display and Adjacent Markets segment grew modestly over the period, growing from $868 million to $916 million. This reflects challenges in the display market, where demand for new manufacturing capacity has been limited.

Fortunately, this segment represents only 3.3% of total revenue, so its impact on the overall business remains limited.

Operating Margin Analysis:

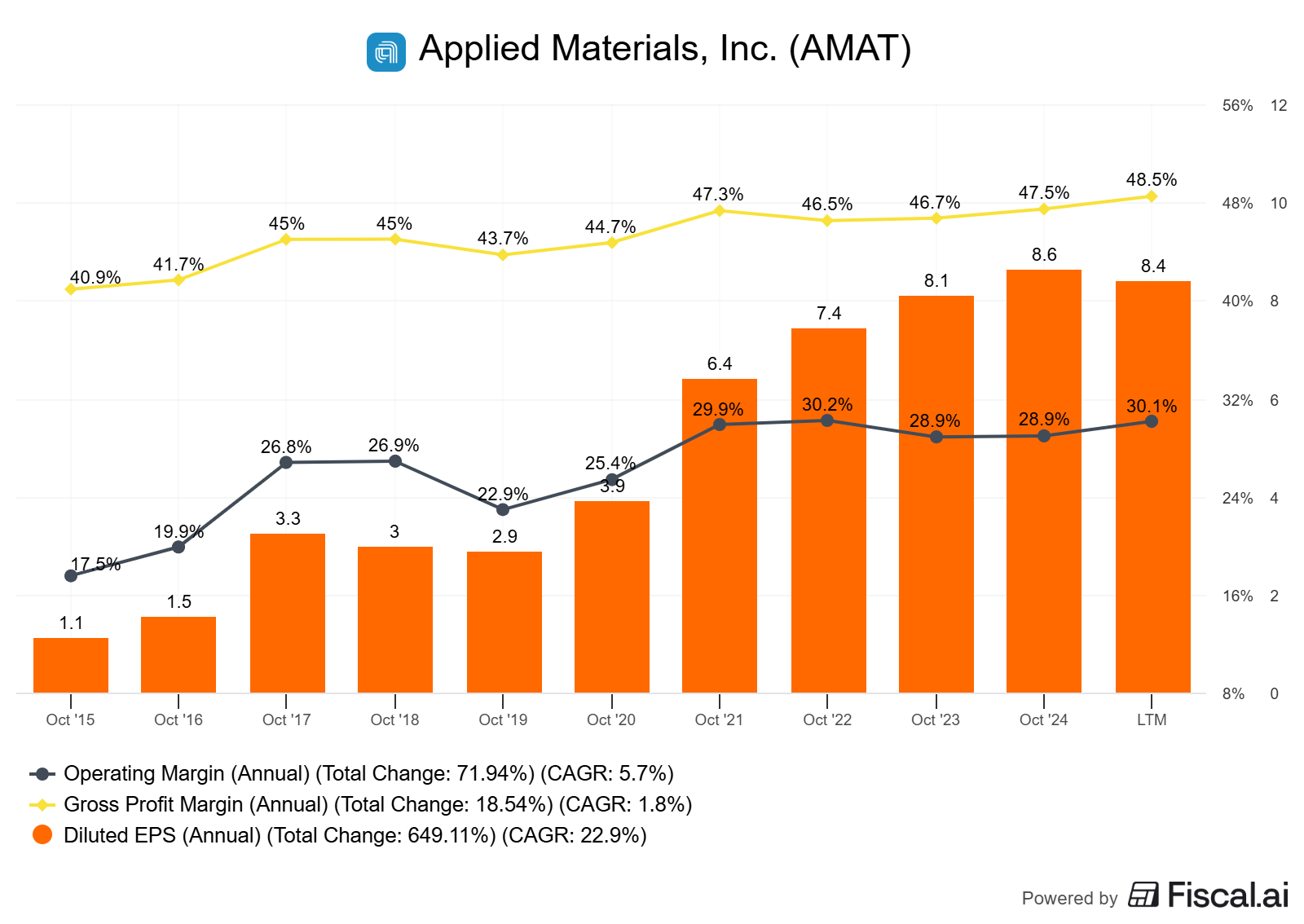

Applied Materials doesn’t break out operating margins by segment in their standard financial statements, but we can look at overall profitability. In fiscal 2024, the company achieved:

Gross margin: 47.5%

Operating margin: 28.9%

Earnings per share: $8.65

These margins compare favorably to many semiconductor companies and reflect the company’s pricing power and operational efficiency.

Comparing Applied Materials to Competitors

To understand Applied Materials’ position, let’s compare it with other semiconductor equipment makers and a fab-less chip designer (NVIDIA) to see how different business models yield different financial results.

Table 2: Company Comparison (November 2025 Data)

Let’s break down what this comparison tells us:

Equipment Makers vs. Chip Designers

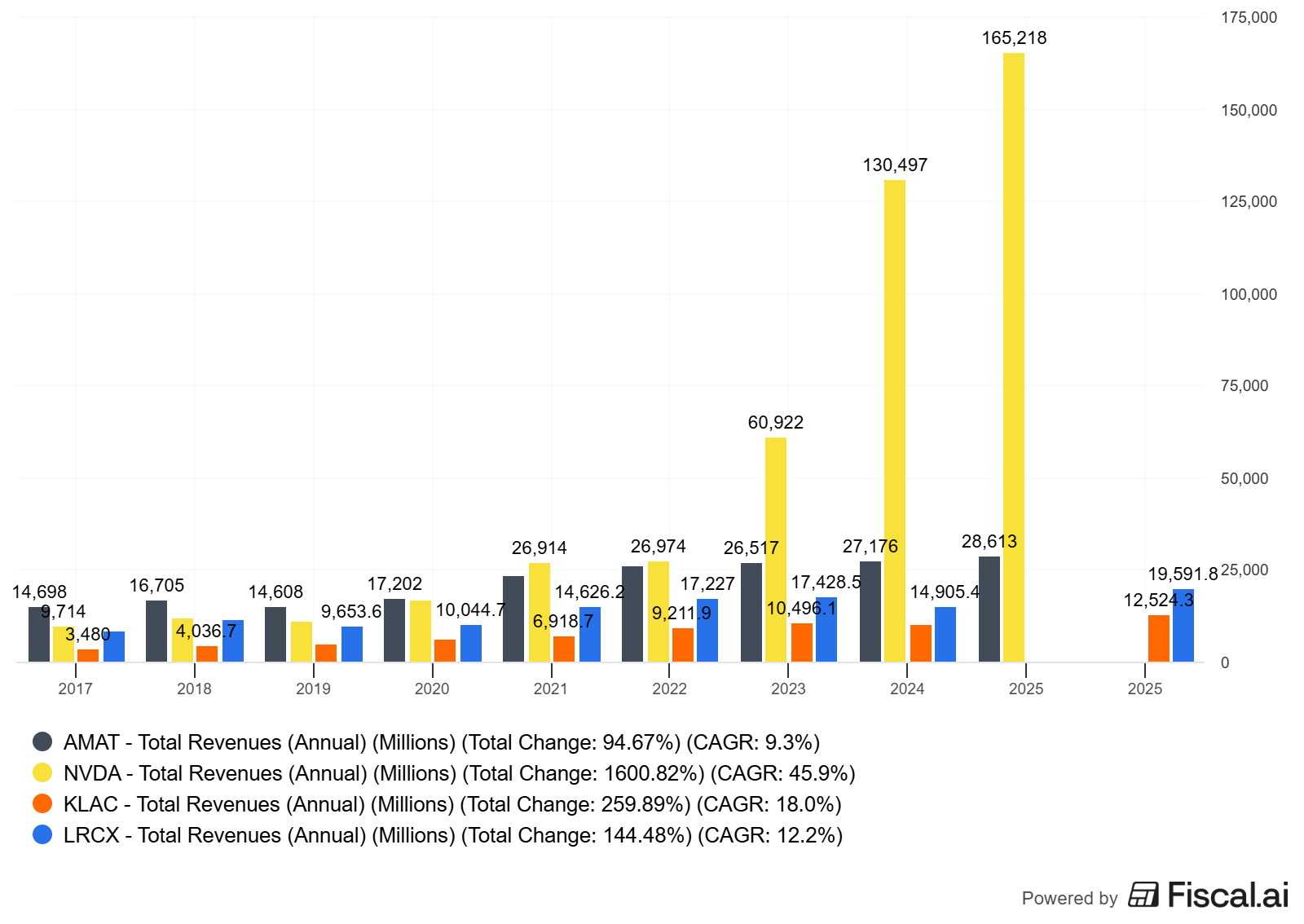

The most striking difference is NVIDIA’s explosive growth. While Applied Materials grew revenue by 7.5% over three years, NVIDIA more than doubled their revenue in fiscal 2024 alone, driven by unprecedented demand for AI chips.

This illustrates a fundamental difference in business models. Chip designers can scale rapidly when demand surges because they don’t need to build factories or manufacture equipment. They design chips and outsource production. Equipment makers like Applied Materials face longer lead times because they need to manufacture complex systems and because their customers (foundries) need time to plan and execute capacity expansions.

However, this cuts both ways. When the AI boom eventually moderates, NVIDIA’s growth will slow much more dramatically than Applied Materials’. Equipment makers benefit from the need for ongoing capacity additions and equipment upgrades, even during slower growth periods.

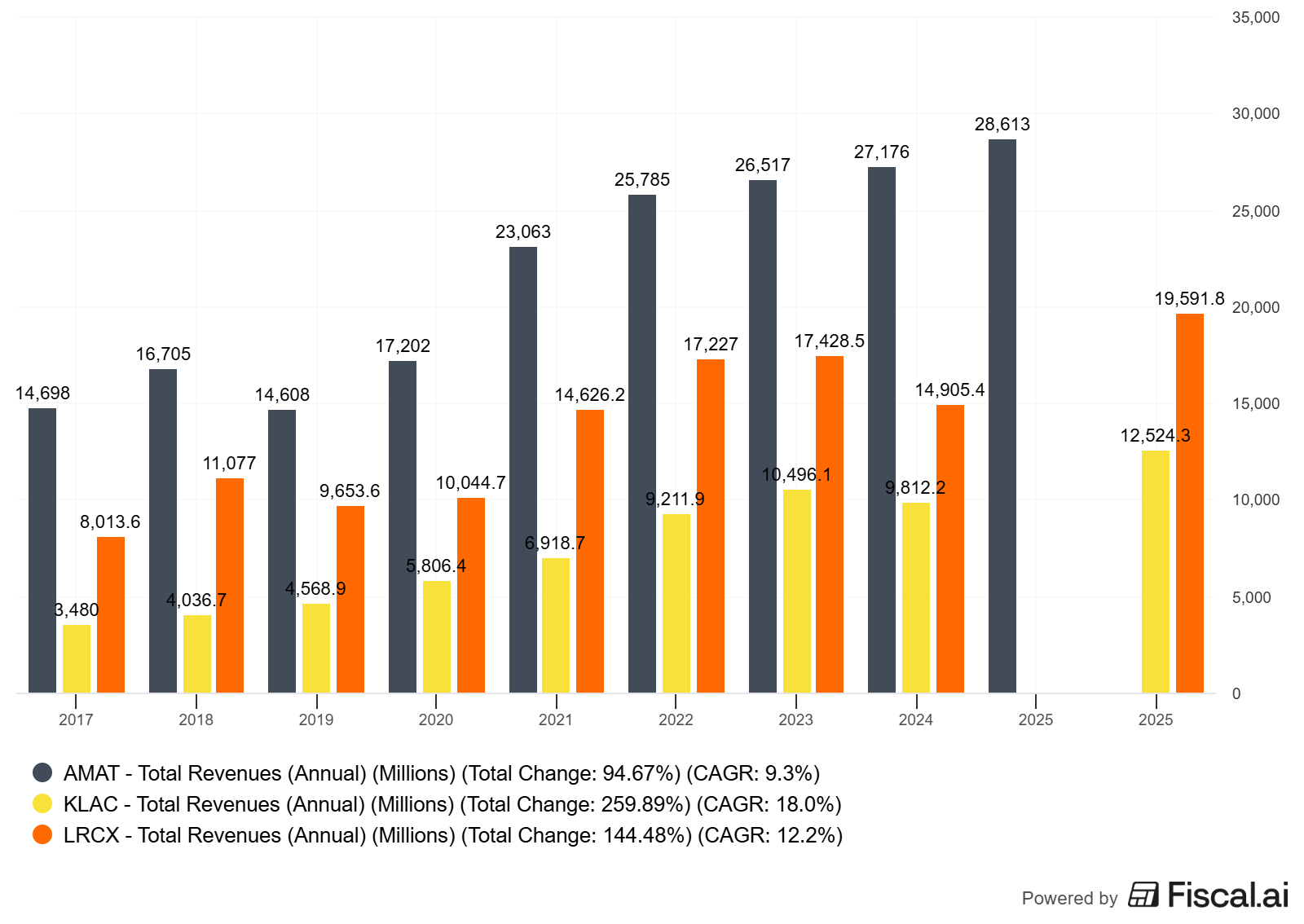

Among Equipment Makers

Comparing Applied Materials to Lam Research and KLA reveals different specializations within the equipment market:

Applied Materials: The broadest portfolio, covering multiple process steps

Lam Research: Specialized in etch and deposition equipment

KLA Corporation: Focused on inspection and metrology

Applied Materials’ broader portfolio provides more diversification across different manufacturing steps. This matters because different parts of the chip manufacturing process require different levels of investment at different times. A company focused on a single process step faces more concentration risk than one serving multiple steps.

The revenue trends also reveal the cyclical nature of the equipment business. Lam Research saw revenue decline from FY2023 to FY2024, then recover in FY2025. KLA followed a similar pattern. Applied Materials showed more stable growth, likely due to their broader portfolio and significant services revenue.

Not too bad, huh?

Applied Materials’ Competitive Moats

Now we get to the heart of the investment case. As Warren Buffett teaches us, we want to invest in businesses with competitive advantages—economic moats that protect their profitability over time.

Applied Materials possesses several significant competitive moats:

1. Technological Leadership

Developing semiconductor manufacturing equipment requires years of research and deep expertise in materials science, physics, chemistry, and engineering.

The equipment needs to work at nanometer scale, processing wafers worth hundreds of thousands of dollars without defects.

This technological complexity creates a substantial barrier to entry. New competitors can’t simply enter the market with cheap alternatives. The equipment either works precisely as required, or it doesn’t work at all.

Applied Materials invests heavily in R&D to maintain this leadership. In fiscal 2024, they spent billions developing next-generation tools for advanced chip architectures like gate-all-around transistors, backside power delivery, and 3D DRAM—technologies that will define the next decade of semiconductor manufacturing.

2. Customer Stickiness and Switching Costs

Once a foundry qualifies Applied Materials equipment in its production process, switching to a competitor proves extremely difficult and expensive. The process qualification alone can take months or years and cost millions of dollars.

More importantly, foundries standardize on specific equipment suppliers to maintain consistency across their fabs. If you’re running 100 Applied Materials deposition systems in one fab, you’ll likely buy Applied Materials for your next fab too. This creates natural customer retention.

3. Installed Base and Recurring Revenue

This brings us back to that Applied Global Services segment. Applied Materials has an installed base of equipment at virtually every major semiconductor manufacturer worldwide. This installed base generates predictable, high-margin service revenue.

As Buffett often says, we want businesses that sell razors and razor blades. Applied Materials sells the “razors” (equipment) and the “razor blades” (spare parts and services). Recurring service revenue provides cash flow stability and reduces the impact of equipment sales cycles.

4. Scale and Scope Advantages

Applied Materials operates at a scale that smaller competitors struggle to match. They can invest in R&D, maintain global service networks, and purchase components at volumes that provide cost advantages.

Their broad portfolio also allows them to sell multiple types of equipment to the same customers, strengthening relationships and providing cross-selling opportunities.

Buffett’s principle of investing in “wonderful businesses at fair prices” applies here. Applied Materials demonstrates many characteristics Buffett looks for: strong competitive positions, recurring revenue, customer relationships that compound over time, and the ability to raise prices as their technology becomes more critical to customers’ operations.

The company’s business quality comes from its competitive moats and recurring service revenue, despite the cyclical nature of equipment sales. This remains a key distinction for investors evaluating the company.

Limitations and Risks

I know we’ve painted a relatively positive picture of Applied Materials, but remember that every business faces limitations and risks. Let’s discuss the key challenges investors need to understand.

1. Cyclicality

This remains the most significant risk for semiconductor equipment makers. Capital equipment purchases by foundries and chip manufacturers follow boom-and-bust cycles. When the industry expands capacity, equipment orders surge. When demand softens or overcapacity develops, orders can drop dramatically.

We saw this pattern in the data earlier. Revenue doesn’t grow in a straight line—it fluctuates based on customer capital spending patterns. This means that, even with recurring service revenue, Applied Materials will experience periods of declining sales and margin pressure.

As investors, we need to accept this cyclicality as part of the business model. The key is buying at reasonable valuations that account for the cyclical nature, rather than extrapolating peak earnings indefinitely.

2. Geopolitical Risk and Export Controls

Applied Materials generates the majority of its revenue from customers outside the United States, with significant exposure to China, Taiwan, and South Korea. This creates multiple geopolitical risks:

Export controls: The U.S. government continues implementing restrictions on selling advanced semiconductor equipment to China. In December 2024, new regulations reduced Applied Materials’ backlog by approximately $549 million.

Taiwan risk: TSMC, one of Applied Materials’ largest customers, operates primarily in Taiwan. Geopolitical tensions between China and Taiwan create uncertainty for the entire semiconductor supply chain.

Trade policy changes: Tariffs, trade restrictions, and shifting government policies can impact Applied Materials’ ability to serve global customers.

These risks remain largely outside of management’s control, making them particularly challenging for investors to assess.

3. Customer Concentration

A handful of large customers—TSMC, Samsung, Intel, and SK Hynix—represent a substantial portion of Applied Materials’ revenue. This customer concentration creates risk. If one major customer significantly reduces capital spending, it can materially impact Applied Materials’ results.

Additionally, these large customers possess significant negotiating power. They can demand pricing concessions, favorable terms, or technology exclusivity that can pressure Applied Materials’ margins.

4. Technology Transition Risk

The semiconductor industry continues evolving rapidly. New manufacturing technologies, different chip architectures, or alternative materials could require entirely different equipment. If Applied Materials fails to develop the right technologies for future chip generations, it could lose market share to competitors.

While their strong R&D spending and customer relationships mitigate this risk, it remains a consideration. The industry has seen established equipment leaders lose ground during major technology transitions.

5. Supply Chain Complexity

Applied Materials doesn’t manufacture every component in-house. They rely on suppliers for specialized parts, materials, and sub-assemblies. Supply chain disruptions, such as those experienced during the COVID-19 pandemic, can delay equipment deliveries and affect revenue recognition.

Investor Takeaway

With that, we will wrap up our discussion today on how Applied Materials makes money.

Applied Materials occupies a critical position in the semiconductor ecosystem as the world's largest supplier of semiconductor manufacturing equipment. Understanding their business model helps investors make more informed decisions about semiconductor investments beyond just chip designers and manufacturers.

The key takeaway remains this: Applied Materials’ business quality comes from its competitive moats and recurring service revenue, despite the cyclical nature of equipment sales.

The company benefits from:

Strong technological leadership in critical manufacturing processes

An installed base generating predictable service revenue

High customer switching costs that create sticky relationships

A diversified portfolio covering multiple manufacturing steps

However, investors must recognize the limitations. The business remains cyclical, with revenue fluctuating based on customer capital spending. Geopolitical risks and export controls create uncertainty. Customer concentration means that major customers wield significant influence.

As Buffett reminds us, focus on businesses with moats and strong long-term economics, but buy them at fair prices that reflect their risks and cyclicality.

Applied Materials meets many criteria for a high-quality business, but, as with all investments, success depends on the price you pay and your time horizon.

FYI, I currently have no position in AMAT.

Remember that our goal as investors remains to understand what we own and why we own it.

By understanding how Applied Materials makes money, through equipment sales and ongoing services to the companies that manufacture the chips powering our modern world, we can make more informed decisions about when and how to invest in this critical part of the technology infrastructure.

As always, thank you for taking the time to read today’s post, and I hope you find something of value in your investing journey. If I can further assist, please don’t hesitate to reach out.

just came across the whole semiconductor landscape several months ago. fascinating stuff.